2035 年稳定币交易量能否接近 1,500 万亿美元?基于 Chainalysis 预测与 2026 年监管现实的情景校验

为什么 “2035 年 1500 万亿美元” 这个预测值得认真讨论

当市场看到 “1500 万亿美元” 这类数字时,第一反应往往是质疑:这个规模是否过于夸张。

但从金融史看,很多关键基础设施在早期都被低估,尤其是同时满足以下条件的系统:

-

具备网络效应,用户越多越好用;

-

具备标准化特征,越标准越容易被机构接入;

-

具备跨市场流通能力,可连接不同资产与司法辖区。

稳定币正在接近这样的临界点。它不再只服务于加密资产交易,而是逐步进入跨境支付、B2B 结算、链上国债、RWA 结算、交易所与托管机构之间的资金清算流程。

因此,讨论这个预测的意义,不是判断某个数字 “会不会精确命中”,而是识别一个更大的方向:全球美元流动性是否正在出现新的分发与结算轨道。

交易量不等于市值,也不等于净新增资金

关于稳定币,经常出现 3 个概念混用,导致判断偏差:

-

市值( Market Cap ):流通中的稳定币存量规模。

-

交易量( Transaction Volume ):在一定周期内链上转移的总金额。

-

净新增资金( Net New Money ):真正新进入体系的资金流入。

如果一个稳定币在机构、交易所、做市商与支付通道之间高频流转,同一笔美元可以在短时间内被多次计入交易量。因此,交易量高并不自动意味着 “新增财富同等规模增长”。

这并不削弱稳定币的重要性,反而说明其可能在承担 “周转效率提升器” 的角色。

换句话说,1500 万亿美元更像是“金融管道吞吐量”的预测,而不是“资产池子大小”的预测。

对从业者而言,最重要的问题应是:这条管道到底在服务哪些真实需求,是否能持续、可审计、可监管地运行。

稳定币交易量增长的 4 个核心驱动

跨境支付与企业财务结算的效率需求

传统跨境支付面临到账慢、链路长、费用不透明等问题。

稳定币的优势在于:

-

7 x 24 小时可用;

-

结算路径更短,减少中间账户层级;

-

对 API 与程序化财务系统更友好。

当企业从 “试点使用” 走向 “流程内嵌”,交易量会从事件驱动转向日常运营驱动。

机构化资金进入链上市场

过去,机构更多通过 ETF 或托管账户接触加密资产。现在,一个新变化是:部分机构开始把稳定币作为链上现金管理工具,用于回购、抵押、短期流动性调配与风险对冲。

一旦稳定币进入机构 Treasury 体系,其交易量将不再只与散户交易热度相关,而与机构资产负债管理节奏相关。

RWA 与链上收益产品扩容

RWA 的核心不是把资产 “上链展示”,而是形成可交易、可结算、可审计的闭环。在这个闭环里,稳定币是最自然的结算单位。

如果链上国债、基金份额、票据类产品持续扩张,稳定币交易量将被动放大,因为每一次资产交割都需要结算媒介。

多链生态与基础设施成熟

过去稳定币活动集中在少数公链。

未来若出现更成熟的跨链消息、统一账户抽象、合规桥接与低成本结算层,稳定币将在更多场景被调用。

这会带来两个结果:

-

单笔交易成本下降,促进高频小额支付;

-

链间资金搬运效率提升,增加总周转。

不能忽视的 5 类约束与风险

乐观叙事成立的前提,是约束条件可被持续管理。以下风险不解决,规模预测就可能被显著下修。

监管碎片化风险

不同地区对稳定币的定义、牌照、储备要求、赎回机制并不一致。

若监管标准长期碎片化,全球流动性会被切割成多个 “区域池”,总交易量增长效率下降。

中心化发行人与托管依赖

主流稳定币仍依赖中心化发行与银行托管。

这意味着存在冻结权限、账户可用性、赎回优先级与对手方风险。

当市场压力上升时,是否能维持 “随时、足额、低摩擦赎回” 是核心压力测试。

链上基础设施与安全风险

跨链桥、预言机、钱包基础设施、合约权限管理仍是攻击高发区。

若高频出现安全事故,机构会提高风险折价,影响真实业务迁移速度。

流动性深度与报价质量不足

有交易量不代表有高质量流动性。

在大额结算场景中,市场更关注以下指标:

-

点差是否可控;

-

深度是否稳定;

-

极端行情下是否仍可成交。

缺乏深度会让稳定币难以承担大规模机构结算功能。

主权数字货币与传统体系竞争

稳定币并非无竞争环境增长。

未来它将面对:

-

传统支付网络的技术升级;

-

商业银行实时清算改造;

-

各类 CBDC 或区域数字结算方案。

因此,稳定币的上限并不由叙事决定,而由其相对效率优势能否持续决定。

从支付工具到结算层:市场结构将如何被重写

稳定币最重要的变化,不是 “更常被用来转账”,而是角色升级。

可以用一个更清晰的路径看待这件事:

-

支付工具阶段:服务 CEX 充提、链上交易、跨境小额转移。

-

结算层阶段:进入企业与机构的标准清结算流程。

-

资金操作系统阶段:与借贷、抵押、风险管理、自动化财务深度耦合。

一旦进入第 2 阶段与第 3 阶段,稳定币交易量会更像 “基础设施流量”,而不是 “市场情绪流量”。

这会带来 3 个结构性影响:

-

对交易所:竞争焦点从 “币种数量” 转向 “清算效率与资金路由能力”。

-

对银行与支付机构:需要重构对链上美元流的监控、风控与对账体系。

-

对加密市场:估值逻辑从单一牛熊叙事,转向基础设施渗透率与现金流可持续性。

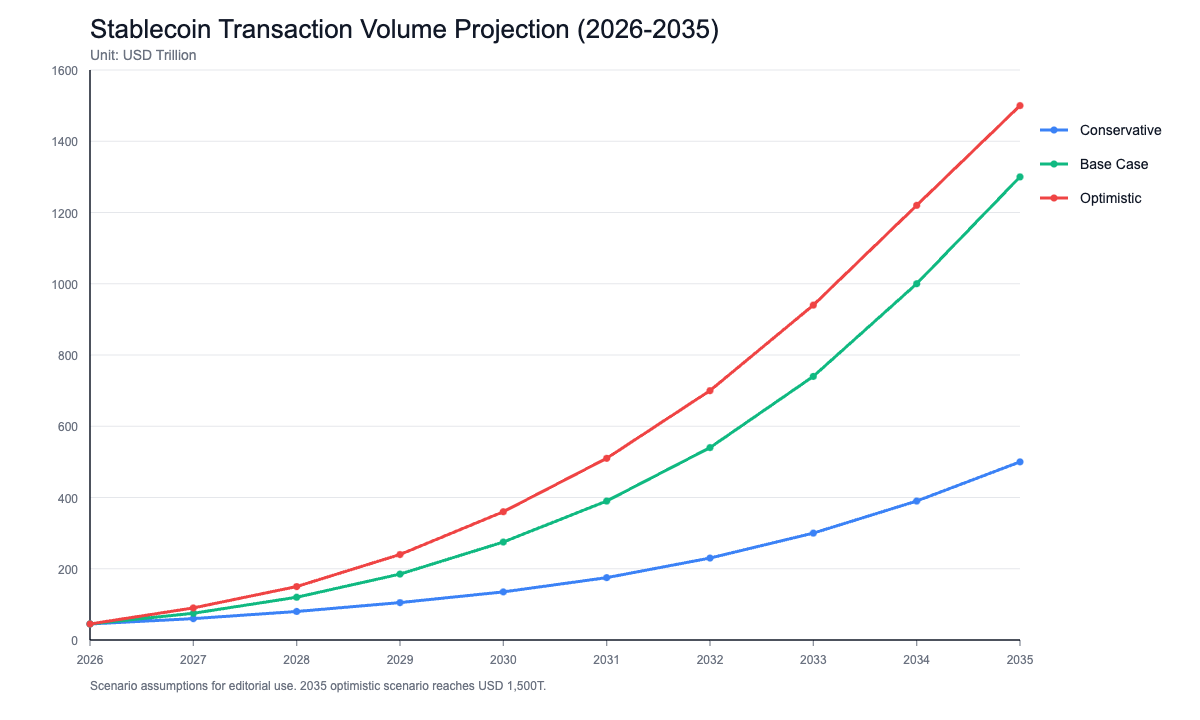

2035 年前的 3 种情景路径与观察指标

为避免 “非黑即白” 判断,可采用情景分析框架。

保守路径( 低于 500 万亿美元 )

-

监管协调缓慢,主要市场标准不统一;

-

机构采用停留在试点层;

-

稳定币主要仍服务加密交易内部周转。

基准路径( 500 万亿 - 1000 万亿美元 )

-

主要经济体形成可互认的合规框架;

-

企业跨境结算和机构 Treasury 使用稳步提升;

-

RWA 与链上现金管理产品持续扩容。

乐观路径( 接近或达到 1500 万亿美元 )

-

稳定币成为跨境结算标准接口之一;

-

多链互操作、审计与合规工具高度成熟;

-

机构将稳定币纳入核心流动性与抵押品体系。

建议持续跟踪以下指标,而非只看单点新闻:

-

稳定币月度活跃地址与大额转账占比;

-

机构级托管与赎回通道数量;

-

合规牌照覆盖范围与跨区域互认进展;

-

稳定币在 RWA 结算中的份额变化;

-

极端行情下的脱锚频率与恢复时间。

结论:稳定币的核心变量不是 “讲故事”,而是 “做基础设施”

“2035 年 1500 万亿美元” 可以被视为一个高位目标,而不是必然结果。

它的价值在于提示市场:稳定币正在从交易工具走向金融基础设施,且这一转变已开始影响支付、清结算、机构资金管理与链上资产发行逻辑。

更客观的判断应当是:

-

短期看,稳定币仍受政策、流动性与风险事件扰动;

-

中期看,稳定币与 RWA、机构化资金、跨境结算的耦合度将持续提高;

-

长期看,真正决定上限的不是叙事热度,而是合规可持续性、技术可靠性与系统级信任。

因此,面对类似 Chainalysis 的长期预测,最专业的态度不是盲目乐观或简单否定,而是回到可验证变量:谁在真实使用、用在什么场景、能否持续低摩擦结算、在压力测试下是否仍可运行。

只要这些问题持续得到正向回答,稳定币交易量在未来 10 年走向更高台阶可以具备现实基础。

分享

目录

相关文章

不可不知的比特币减半及其重要性

如何选择比特币钱包?

CKB:闪电网络促新局,落地场景需发力

Master Protocol:激活 BTC 生息潜力