還記得香港推出自家比特幣與以太坊現貨 ETF 嗎?截至目前,整體交易規模仍顯有限,尚未對市場產生明顯影響力。2024 年 4 月 30 日上市首日,6 檔虛擬資產現貨 ETF 合計成交額低於 1 億港幣,這一數字在美國市場幾乎不會引起任何波瀾。(1)

截至今日,6 檔 ETF 的總資產規模約 3.33 億美元,距離彭博分析師原先預期的「10 億美元」目標仍有不小差距。同期間,美國比特幣現貨 ETF 累計淨流入已超過 560 億美元,管理資產規模近 900 億美元。香港 ETF 規模甚至不及美國的零頭。(2)

但若因此認定香港虛擬資產政策僅止於「雷聲大、雨點小」,您或許忽略了水面下的深層變化。

ETF 交易量雖然尷尬,香港真正的 crypto 故事其實並不在 ETF K 線圖上,而在於牌照發放進度、傳統金融機構入場深度,以及 RWA 代幣化從沙盒走向實際落地的進程。

交易基礎設施:從 2 家到 12 家,牌照爆發式成長

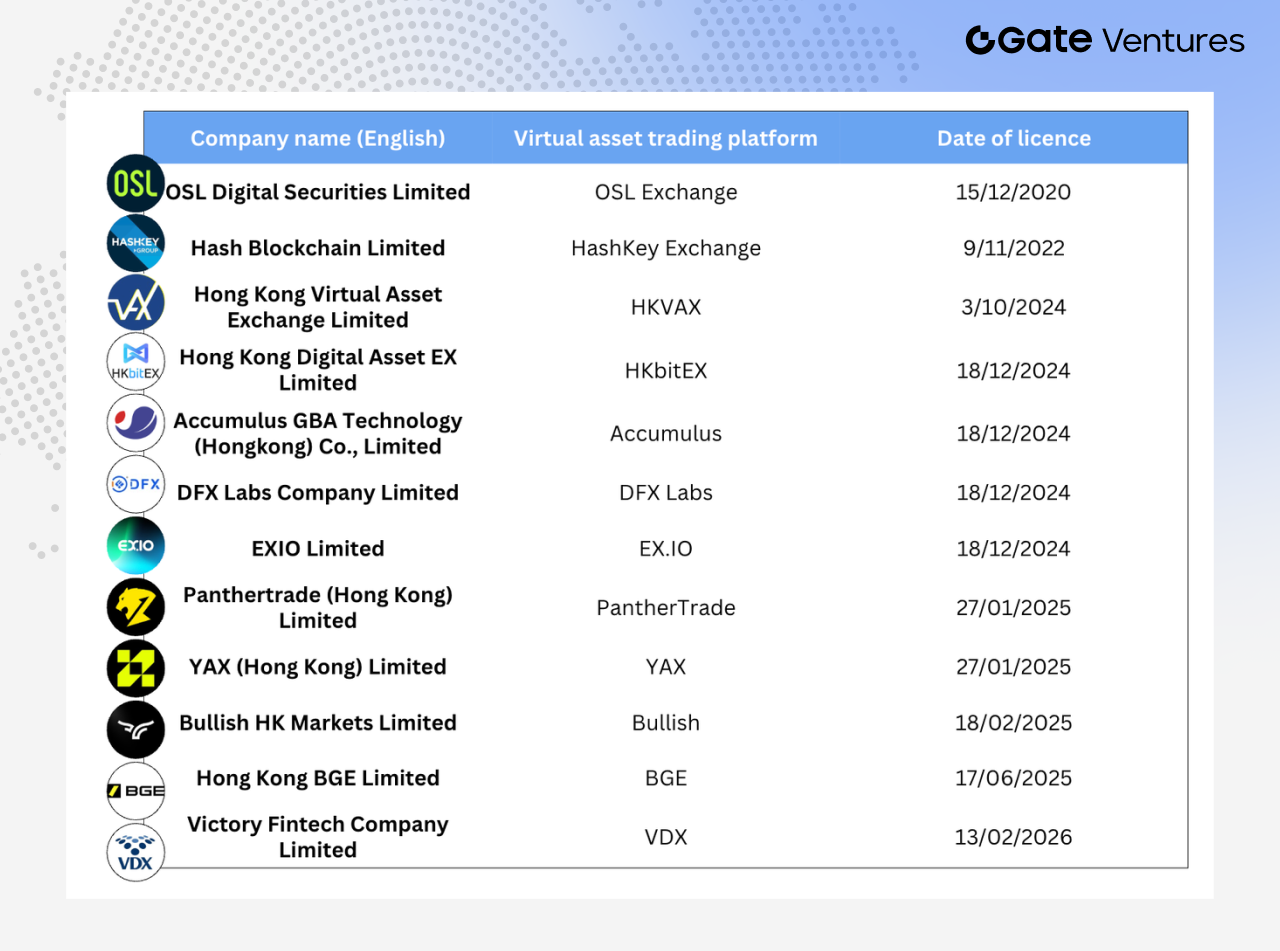

2023 年香港證監會(SFC)首次批准虛擬資產交易平台時,僅有 OSL 與 HashKey 兩家取得牌照。這兩家是最早的先行者,也是唯一能向零售客戶提供加密貨幣交易服務的平台。

至 2025 年中,持牌虛擬資產交易平台(VATP)數量已擴大至 12 家。

值得關注的是新入場者的背景構成。12 家平台中,有 4 家來自互聯網券商陣營:

- 富途證券全資子公司獵豹交易(PantherTrade)於 2025 年 1 月獲 VATP 牌照

- 老虎國際旗下 YAX (Hong Kong)

- 新浪旗下華盛資本投資的 EXIO

- 勝利證券旗下 VDX

此外,還包括 Bullish HK Markets(即 Peter Thiel 投資的加密交易所 Bullish 香港實體)、DFX Labs 等。

從「1 號牌升級」到專屬 VA 牌照:監管範式全面革新

2025 年上半年,傳統券商集體升級 1 號牌進入虛擬資產賽道的新聞引發市場熱議。超過 42 家機構獲批,通過綜合帳戶安排提供虛擬資產交易服務,包括國泰君安國際、富途證券(香港)、盈透證券、眾安銀行等悉數入場。2025 年 6 月,國泰君安國際更取得「虛擬資產全牌照」,消息公布次日港股暴漲近 200%。(3)

不過,這套「1 號牌升級」框架,本質上只是現有《證券及期貨條例》(SFO)牌照體系的延伸與附加,並非獨立、完整的虛擬資產中介監管制度。券商仍須通過綜合帳戶於持牌交易所(如 HashKey)執行交易,採預先注資安排,零售客戶可交易範圍基本限於大市值代幣,資產託管則主要依賴交易所或銀行體系。

同時,相關規則分散於聯合通函、附錄條款及個別牌照條件,整體合規架構仍顯零散,制度整合度有限。

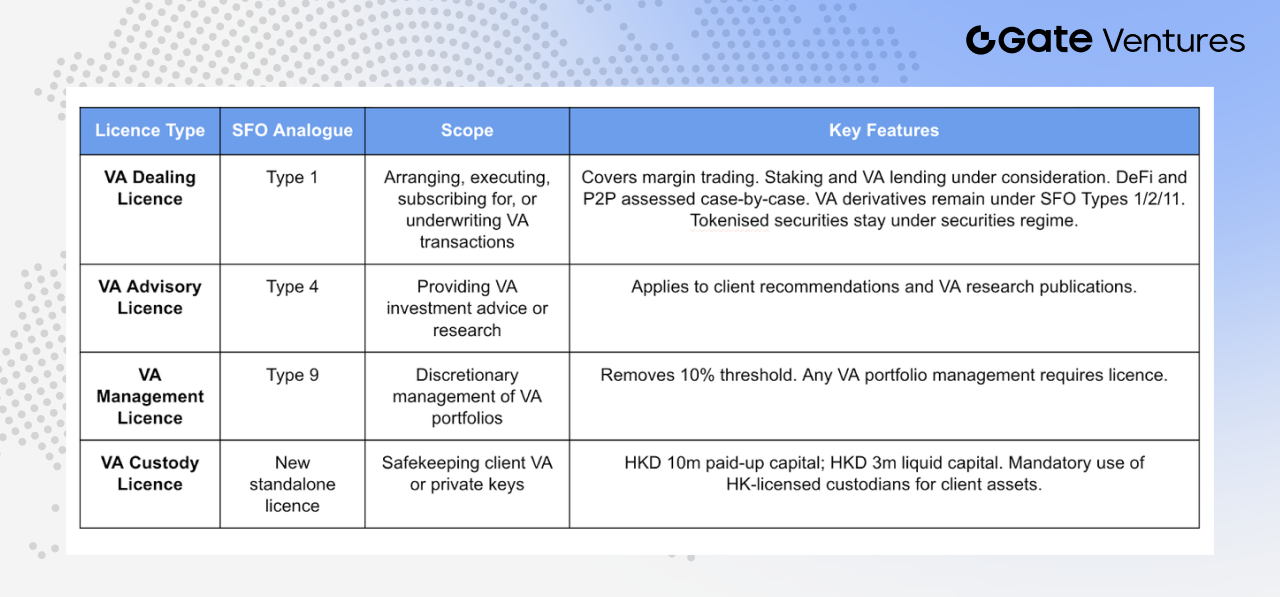

真正的轉捩點出現在 2025 年 12 月 24 日。財經事務及庫務局(FSTB)和證監會聯合發布諮詢總結,正式敲定一套全新、專為虛擬資產量身打造的牌照制度,納入《打擊洗錢及恐怖分子資金籌集條例》(AMLO)架構,立法目標定於 2026 年。同日並啟動為期一個月的進一步諮詢,涵蓋虛擬資產投資諮詢及資產管理牌照。

新框架將虛擬資產業務細分為四大獨立牌照類別:

-

虛擬資產交易牌照(VA Dealing):對應現行《證券及期貨條例》(SFO)1 號牌(證券交易),涵蓋業務過程中促成虛擬資產買賣、認購或包銷安排等行為。 涵蓋範圍包括保證金交易、質押、虛擬資產借貸,以及去中心化平台和 P2P 交易模式等。至於虛擬資產衍生品(如期貨及結構性產品),則繼續納入 SFO 第 1、2 及 11 號牌監管;代幣化證券亦維持於現行證券監管體系下,避免監管重疊。

-

虛擬資產投資諮詢牌照(VA Advisory):對應 SFO 第 4 號牌,適用於向客戶提供虛擬資產買賣建議,或發布與虛擬資產投資相關研究報告、分析意見的行為。

-

虛擬資產資產管理牌照(VA Management):對應 SFO 第 9 號牌,適用於全權管理客戶虛擬資產投資組合。關鍵變革在於取消原有 10% 最低門檻(de minimis threshold)。 舊制下,僅當投資組合中虛擬資產占比超過總資產 10% 時才需觸發升級監管要求;新制明定,只要涉及虛擬資產投資組合管理,無論占比多少,均須取得專屬牌照,消除因市場波動被動「超標」的監管灰色地帶。

-

虛擬資產託管牌照(VA Custody):全新設立的獨立牌照,適用於負責保管、控制或管理客戶虛擬資產轉移工具(通常為私鑰)的機構。 最低資本要求為實繳股本不少於 1,000 萬港元,以及 300 萬港元以上的流動資金。同時,虛擬資產交易商須將客戶資產託管於設於香港並持有證監會牌照的虛擬資產託管機構,形成強制本地化託管,降低跨境託管執行風險。

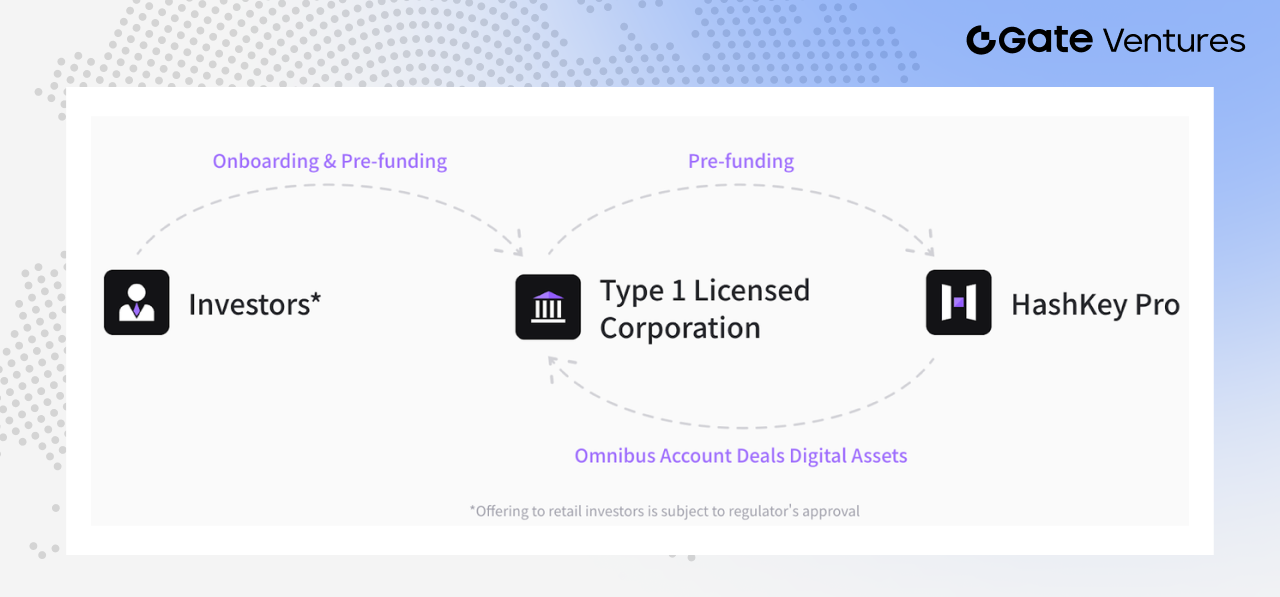

HashKey 的「樞紐」角色

Source: Hashkey Pro Docs

在現有生態中,HashKey Exchange 充當基礎設施樞紐。2025 年 6 月,HashKey 宣布其 Omnibus 綜合帳戶服務已覆蓋 90% 持牌券商,為逾 30 家機構提供虛擬資產交易、託管及交割服務,包括國泰君安國際、富途、老虎等。換句話說,多數券商的加密交易最終都在底層由 HashKey 完成。(4)

RWA 代幣化:從構想走向實戰

與現貨 ETF 及交易平台牌照目前尚未形成明顯規模效應、應用場景有限相比,RWA 及代幣化資產發展更具落地性。

2024 年 8 月,香港金管局啟動 Project Ensemble 沙盒,首輪聚焦四大方向:固定收益與投資基金、流動性管理、綠色金融,以及貿易及供應鏈金融。其後,香港市場陸續出現多宗具代表性的代幣化與 RWA 項目,顯示應用正從概念驗證走向實際落地。

新能源領域方面,朗新集團與螞蟻數科以充電樁收益權為底層資產,完成約 1 億元人民幣的跨境 RWA 融資;協鑫能科亦與螞蟻數科合作,將光伏資產收益權上鏈,完成逾 2 億元人民幣融資。巡鷹集團也積極推進兩輪車換電資產相關 RWA 探索,反映應用場景逐步擴大。(5)

基金產品進展同樣顯著。華夏基金(香港)於 2025 年 2 月推出港元代幣化貨幣市場基金,被視為亞太首批面向零售投資者的代幣化基金,首發規模約 1.07 億至 1.1 億美元,並經由 OSL、富途等渠道分銷。(6)

2025 年 3 月,博時基金(國際)與 HashKey 合作的港元與美元貨幣市場 ETF 代幣化份額獲證監會批准。2025 年 7 月,華夏基金(香港)再推美元及人民幣代幣化貨幣市場基金,其中人民幣基金被報導為全球首檔人民幣計價代幣化基金。(7)

至 2025 年下半年,RWA 應用範圍由新能源拓展至更多領域。德林控股宣布與 Asseto 合作,探索最高 5 億港元規模的實體資產代幣化,涵蓋物業權益及基金資產;翰宇藥業與 KuCoin 簽署合作意向,計畫於香港開展以創新藥未來收益權為底層資產的 RWA 試點;另有醫療與地產相關企業探索知識產權及商業地產代幣化。

近期市場亦出現貴金屬資產代幣化案例,包括艾德金融統籌發行的白銀代幣,以及 EX.IO 上架的 LBMA 認證實物黃金鏈上黃金代幣 XAUM,顯示 RWA 場景正延伸至大宗商品資產領域。(8)(9)

此外,Esperanza 證券於獲監管許可下,推出兩個代幣化娛樂投資項目,包括紅館香港舉行的《黃凱芹 40 年來香港演唱會 2026》,與馬來西亞舉行的韓國男團演唱會。整體而言,案例顯示代幣化資產範圍持續擴展。(10)

香港政府代幣化債券:試點走向常態化

若說企業、基金端的代幣化仍在擴展,香港政府代幣化債券的發展則更明確反映官方推動其制度化。

Source: Nomura

香港政府已完成多輪代幣化政府債券發行。2025 年第四季,特區政府發行第三批代幣化綠色債券,規模達 100 億港元。其後,當局明確表示,代幣化債券將逐步常態化發行。

2026–27 年度財政預算案中,財政司司長陳茂波提出,由金管局全資附屬機構 CMU OmniClear 控股公司開發專屬數位資產平台,用於支持代幣化債券之發行、登記及結算,並逐步擴展至更多數位資產類型。(11)

這顯示,代幣化債券在香港已非一次性創新試驗,而是納入長期金融基礎設施建設。

CMU OmniClear:代幣化債券基礎設施載體

CMU OmniClear 為香港債券中央託管與結算系統 CMU 的營運機構,CMU 本身即為政府債券發行及結算體系的核心基礎設施。

換言之,無論傳統或代幣化政府債券,其登記、託管與結算均依託 CMU 系統進行。將代幣化債券納入 CMU OmniClear 平台,並非另起爐灶,而是讓數位證券直接接入現有香港債券發行與結算系統。

這項安排的意義主要體現在三方面:

- 流程標準化:代幣化債券納入成熟結算體系

- 監管明確:金管局體系直接參與推動與監督

- 規模易於擴大:平台自始即針對機構級場景設計

隨著港交所於 2025 年 11 月入股 CMU OmniClear 控股公司並持股 20%,此平台亦被視為推動香港固定收益及貨幣市場發展的重要基礎設施。(12)

總體而言,香港代幣化發展已逐步形成兩條主線:一為企業、基金及多元實體資產的市場化探索,另一則是以政府債券與核心金融基礎設施為基礎的制度化建設。後者尤為值得關注,因為這意味著代幣化正逐步進入香港金融體系核心。

穩定幣立法:打通 RWA「最後一公里」

RWA 代幣化始終面臨結構性問題:資產在鏈上,資金仍在線下。

雖然底層資產可完成數位化上鏈,但融資、申購贖回及收益分配等關鍵環節,仍多依賴傳統法幣體系,鏈上與鏈下尚未真正形成閉環。穩定幣正是打通這一閉環的關鍵基礎設施。

2025 年 5 月 21 日,香港立法會三讀通過《穩定幣條例草案》,並於 2025 年 8 月 1 日正式生效。核心規範包括:

- 發行人必須為香港註冊實體,最低實繳股本 2,500 萬港元

- 儲備資產須 100% 覆蓋流通量,並與自有資產嚴格隔離託管

- 持有人享有按面值贖回的法定權利

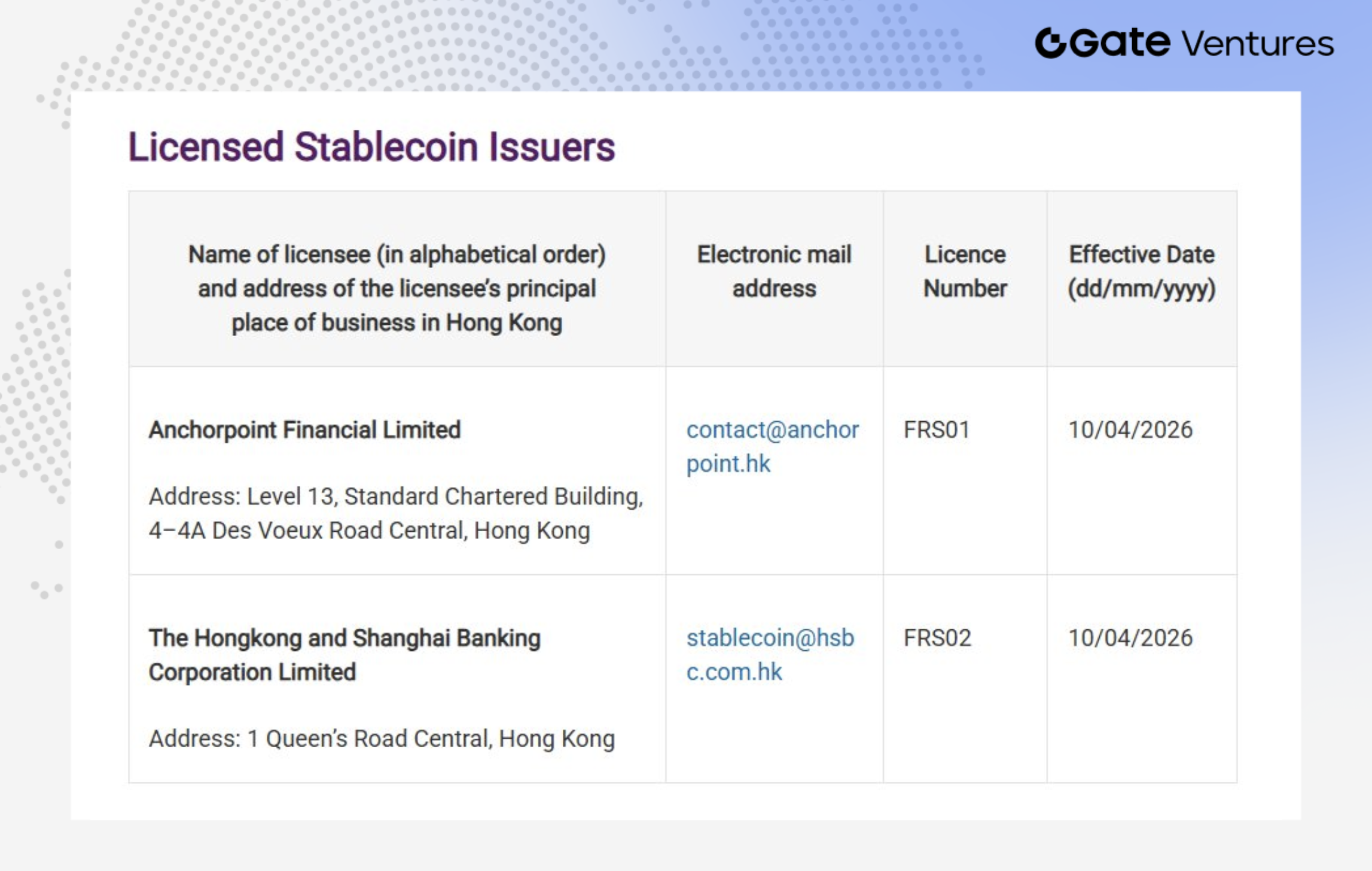

Source: HKMA(截至 2026 年 2 月 4 日)

市場布局方面,香港金融管理局已發出首兩張穩定幣發行人牌照,分別授予香港上海匯豐銀行有限公司,以及 Anchorpoint Financial Limited——後者由渣打銀行、Animoca Brands 與香港電訊合資設立。(13)

匯豐表示,計畫以此次獲牌為契機,於 2026 年下半年推出港元穩定幣,並接入 PayMe 及 HSBC HK App 兩大本地數位渠道。初期應用場景主要包括:一、個人對個人轉帳(P2P),用戶可透過 PayMe 及 HSBC HK App 以穩定幣即時轉帳;二、個人對商戶支付(P2M),用戶可透過 PayMe 以穩定幣向參與商戶付款;三、代幣化投資,透過 HSBC HK App 以穩定幣認購代幣化投資產品。

渣打則表示,Anchorpoint Financial Limited 預計於今年第二季起分階段推出受監管、與港元掛鉤的穩定幣 HKDAP。業務模式上,安點金融將採 B2B2C 路徑,透過指定認可分銷商的現有客戶網路擴大觸達,推動 HKDAP 廣泛進入零售及支付場景。

從兩家機構的市場推進路徑觀察,現階段穩定幣更像底層結算基礎設施,而非直接面向用戶銷售的產品。對終端用戶而言,感知度未必明顯,更多體現在優化支付與清算流程,如降低交易成本、提升資金劃轉效率,並推動「交易即結算」體驗。

其次,香港零售端對穩定幣的實際採用仍處早期,需求與使用習慣尚未完全形成,能否快速打開大眾市場仍有待觀察。當前分發渠道明顯以銀行、持牌機構及其合作網路為主,市場拓展路徑以機構主導,尚未出現由零售端自發擴散的趨勢。

因此,無論產品推出節奏、用戶覆蓋範圍或實際滲透效率,目前仍存較大不確定性。整體而言,香港穩定幣市場雖已進入落地階段,但商業化進展與零售普及度仍屬早期探索期。

全局冷靜檢視:差距何在?

至此,仍需客觀面對幾個關鍵問題:

-

ETF 規模落差極大。 截至今日,香港 6 檔虛擬資產 ETF 總規模僅約 3.33 億美元,同期美國比特幣 ETF 管理資產近 900 億美元,累計淨流入超 560 億美元,規模差距達兩個數量級。

-

RWA 項目多處於沙盒或私募階段。儘管朗新充電樁、協鑫光伏等案例具示範意義,整體融資規模多停留於 1–2 億元人民幣區間,距離「兆美元級代幣化資產」市場願景仍有明顯差距。

大宗商品代幣化方面,需求端發展亦存不確定性。以美國市場為例,代幣化黃金已納入鏈上抵押、槓桿借貸等 DeFi 應用,對零售投資者開放,形成一定生態。相較之下,香港相關產品多以專業投資者為主,零售端參與渠道尚未完全打開,體現政策層面對投資者保護的審慎取向。

- 「鏈上資產、鏈下資金」的斷點尚未完全解決。 穩定幣條例雖已落地,合規穩定幣從「有法規」走向「廣泛應用」仍有一段路。

接下來市場關注的不僅是牌照發放,而是穩定幣能否率先於哪些場景真正落地。較具現實性的應用方向包括:跨境支付與資金劃轉、鏈上資產交易結算、代幣化基金或債券申購贖回,以及企業或平台內部現金管理與清算安排。

這些場景有助於解決 RWA 當前「資產在鏈上、資金在線下」的結構性斷點。香港金管局亦明確表示,首批牌照數量極少,申請人需證明具明確使用場景、穩健營運能力與可信商業模式,顯示監管更關注「能否落地」,而非僅「發幣」本身。

主要數據來源:

-

https://www.21jingji.com/article/20250626/herald/7a7d09161b82588b801777a3d6f713db.html

-

https://www.21jingji.com/article/20250710/herald/10533d03952cd28b3c08f3be0ea28e1b.html

-

https://www.chinaamc.com.hk/zh-hant/product/chinaamc-hkd-digital-money-market-fund/

-

https://phemex.com/news/article/exio-launches-xaum-gold-token-for-professional-investors-57051

-

https://www.hkex.com.hk/News/News-Release/2025/251112news?sc_lang=zh-HK

關於 Gate Ventures

Gate Ventures 隸屬 Gate 集團,是專注於去中心化基礎設施、生態系統及應用程式投資的風險投資部門,致力於重塑 Web 3.0 時代格局。Gate Ventures 與全球產業領袖深度合作,賦能具創新思維與能力的團隊和新創企業,重新定義社會與金融的互動模式。

如需進一步資訊,請瀏覽:官網 | X | Telegram | 領英 | Medium

免責聲明: 本內容不構成任何邀約、招攬或建議。您在做出任何投資決策前應始終尋求獨立專業意見。請注意,GateVentures 可能限制或禁止受限制地區的所有或部分服務。詳情請參閱用戶協議,連結:https://www.gate.com/zh/user-agreement。

分享

相關文章

鏈上 TCG 如何引領下一個 20 億美元市場:產業格局解析與估值前景

Gate Ventures 本週加密貨幣回顧(2025 年 9 月 22 日)

Gate Ventures 每週加密貨幣回顧(2025年8月25日)

深度研究:前景分析——美聯儲結束量化緊縮時機及其對加密市場潛在影響

Gate Ventures 本週加密市場回顧(2025年 8 月 18 日)