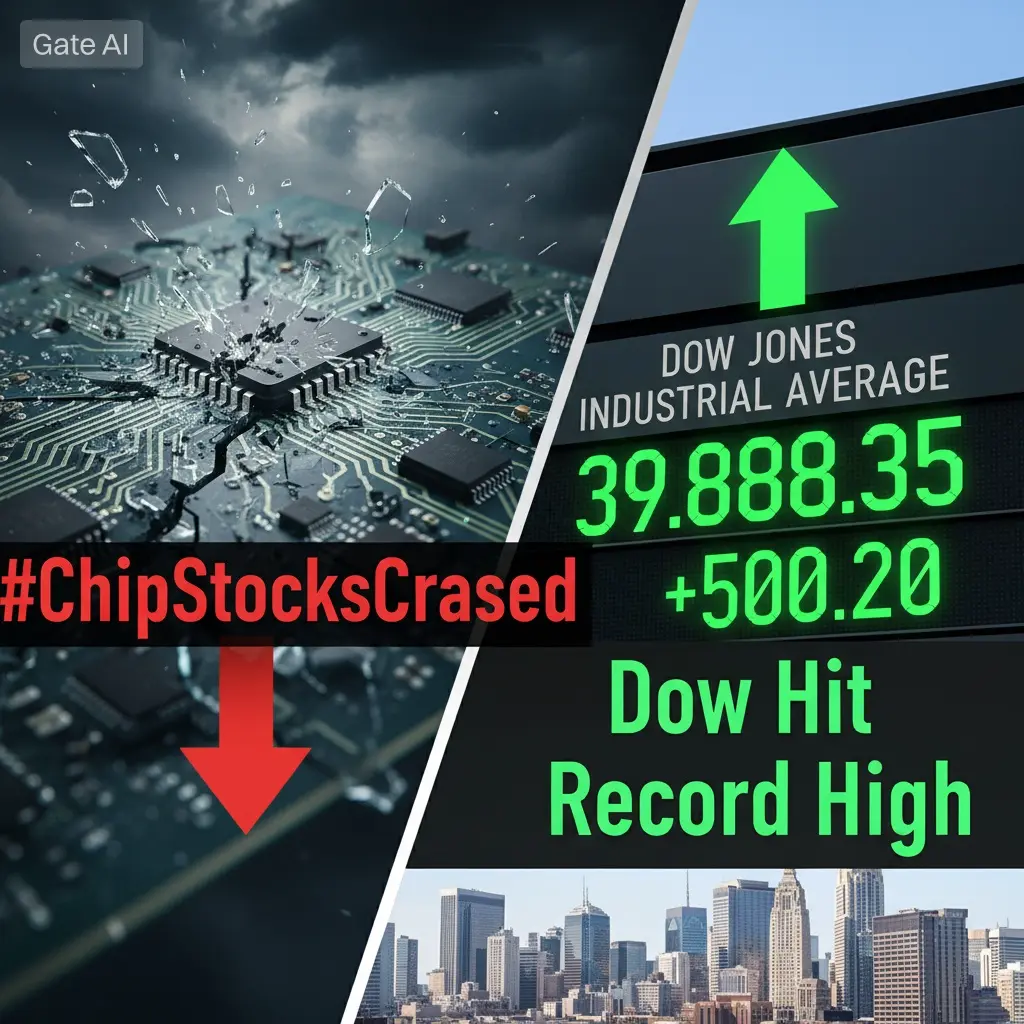

#ChipStocksCrashedDowHitRecordHigh

Chip Stocks Crash While Dow Hits Record High: The Great Rotation Unfolds

The AI Trade Unravels

Thursday, June 4, 2026 will be remembered as the day the artificial intelligence trade finally took a breath—and the divergence between growth and value reached historic proportions. Broadcom, the semiconductor heavyweight that had ridden the AI wave to a 38% gain this year, plummeted over 11% in a single session, shedding approximately $286 billion in market capitalization. This wasn't just a correction; it was a reality check that rippled through the entire chip ecosystem.

The catalyst was disappointingly straightforward: Broadcom's AI chip revenue guidance of $16 billion fell short of the $17.2 billion analysts had expected, despite delivering a quarter that would have been considered stellar in any other context. CEO Hock Tan attempted to reassure investors by reiterating the company's long-term target of $100 billion in AI semiconductor revenue, but markets had already made their judgment. When expectations are priced for perfection, merely being excellent becomes a sin.

The contagion spread rapidly through the semiconductor complex. Micron Technology, a critical supplier of high-bandwidth memory for AI accelerators, cratered 7% as investors recalibrated AI capital expenditure expectations across the entire supply chain. Arm Holdings and other chip names joined the selloff, pushing the Philadelphia Semiconductor Index down more than 2%. This wasn't isolated weakness—it was a wholesale repricing of AI infrastructure demand.

The Blue Chip Renaissance

While technology burned, traditional American industry soared. The Dow Jones Industrial Average surged nearly 810 points to close at 51,496—a record high that capped one of the most dramatic sector rotations in recent memory. Healthcare and financial stocks, long dismissed as boring by AI-obsessed investors, suddenly became the belles of the ball.

UnitedHealth Group led the charge with a 3% gain after Bank of America upgraded the healthcare conglomerate to "buy," citing resilience and defensive characteristics that suddenly mattered again. Financial heavyweights including Goldman Sachs, JPMorgan Chase, Morgan Stanley, and Bank of America all hit fresh 52-week highs, their strong balance sheets and robust lending margins offering shelter in a storm of tech volatility.

The divergence was stark and unprecedented: nine of eleven S&P 500 sectors finished in positive territory, while technology—the sector that had carried markets for three consecutive years—became the sole laggard. The S&P 500 managed a modest 0.53% gain, and the Nasdaq Composite barely eked out a 0.23% advance, held back entirely by the crushing weight of chip stocks.

What This Rotation Tells Us

This wasn't merely profit-taking; it was a fundamental repricing of risk. For years, investors had paid any price for exposure to AI infrastructure, convinced that demand would justify valuations regardless of near-term profitability. Broadcom's guidance miss exposed the fragility of that assumption—when expectations become unmoored from reality, even strong results cannot satisfy.

The rotation into healthcare and financials reflects something deeper: a recognition that economic resilience matters. Healthcare offers demographic tailwinds and recession-resistant cash flows. Banks benefit from normalized interest rates and strong balance sheets. These are real businesses generating real profits today, not promises of transformative growth tomorrow.

Key Levels and Technical Significance

From a technical perspective, several levels now demand attention. Broadcom's $410 handle represents a critical support zone—having closed near $479 the previous session, the stock now sits more than 14% lower. The $400 psychological level becomes pivotal; a sustained break below could trigger further liquidation from momentum strategies that had piled into the name.

For the Dow, 51,500 emerges as the new frontier. The index's ability to sustain this breakout will determine whether this rotation has legs or represents a temporary rebalancing. Healthcare's breakout above resistance and financials' push to 52-week highs suggest institutional capital is genuinely redeploying, not merely parking on the sidelines.

The Philadelphia Semiconductor Index's decline through key moving averages signals that chip stocks may face continued pressure. With the index down over 2% while the broader market rallied, relative strength has definitively shifted away from the group that led markets since 2023.

Investment Implications

This rotation presents both danger and opportunity. Investors overweight in AI-adjacent names face the uncomfortable reality that even companies beating earnings can see double-digit declines if guidance disappoints. The margin for error has vanished.

Conversely, value-oriented sectors that had lagged the AI boom now offer asymmetric upside. Healthcare's combination of defensive characteristics and AI adoption potential makes it particularly compelling—companies that can demonstrate quality business models while participating in the AI revolution may be the true winners of the next phase.

The market is sending a clear message: growth at any price is no longer acceptable. As we enter a period where profitability, balance sheet strength, and cash generation regain importance, the rotation from tech to traditional industry may only be beginning. The AI revolution is real, but the market has finally started asking the right question—at what price?

Chip Stocks Crash While Dow Hits Record High: The Great Rotation Unfolds

The AI Trade Unravels

Thursday, June 4, 2026 will be remembered as the day the artificial intelligence trade finally took a breath—and the divergence between growth and value reached historic proportions. Broadcom, the semiconductor heavyweight that had ridden the AI wave to a 38% gain this year, plummeted over 11% in a single session, shedding approximately $286 billion in market capitalization. This wasn't just a correction; it was a reality check that rippled through the entire chip ecosystem.

The catalyst was disappointingly straightforward: Broadcom's AI chip revenue guidance of $16 billion fell short of the $17.2 billion analysts had expected, despite delivering a quarter that would have been considered stellar in any other context. CEO Hock Tan attempted to reassure investors by reiterating the company's long-term target of $100 billion in AI semiconductor revenue, but markets had already made their judgment. When expectations are priced for perfection, merely being excellent becomes a sin.

The contagion spread rapidly through the semiconductor complex. Micron Technology, a critical supplier of high-bandwidth memory for AI accelerators, cratered 7% as investors recalibrated AI capital expenditure expectations across the entire supply chain. Arm Holdings and other chip names joined the selloff, pushing the Philadelphia Semiconductor Index down more than 2%. This wasn't isolated weakness—it was a wholesale repricing of AI infrastructure demand.

The Blue Chip Renaissance

While technology burned, traditional American industry soared. The Dow Jones Industrial Average surged nearly 810 points to close at 51,496—a record high that capped one of the most dramatic sector rotations in recent memory. Healthcare and financial stocks, long dismissed as boring by AI-obsessed investors, suddenly became the belles of the ball.

UnitedHealth Group led the charge with a 3% gain after Bank of America upgraded the healthcare conglomerate to "buy," citing resilience and defensive characteristics that suddenly mattered again. Financial heavyweights including Goldman Sachs, JPMorgan Chase, Morgan Stanley, and Bank of America all hit fresh 52-week highs, their strong balance sheets and robust lending margins offering shelter in a storm of tech volatility.

The divergence was stark and unprecedented: nine of eleven S&P 500 sectors finished in positive territory, while technology—the sector that had carried markets for three consecutive years—became the sole laggard. The S&P 500 managed a modest 0.53% gain, and the Nasdaq Composite barely eked out a 0.23% advance, held back entirely by the crushing weight of chip stocks.

What This Rotation Tells Us

This wasn't merely profit-taking; it was a fundamental repricing of risk. For years, investors had paid any price for exposure to AI infrastructure, convinced that demand would justify valuations regardless of near-term profitability. Broadcom's guidance miss exposed the fragility of that assumption—when expectations become unmoored from reality, even strong results cannot satisfy.

The rotation into healthcare and financials reflects something deeper: a recognition that economic resilience matters. Healthcare offers demographic tailwinds and recession-resistant cash flows. Banks benefit from normalized interest rates and strong balance sheets. These are real businesses generating real profits today, not promises of transformative growth tomorrow.

Key Levels and Technical Significance

From a technical perspective, several levels now demand attention. Broadcom's $410 handle represents a critical support zone—having closed near $479 the previous session, the stock now sits more than 14% lower. The $400 psychological level becomes pivotal; a sustained break below could trigger further liquidation from momentum strategies that had piled into the name.

For the Dow, 51,500 emerges as the new frontier. The index's ability to sustain this breakout will determine whether this rotation has legs or represents a temporary rebalancing. Healthcare's breakout above resistance and financials' push to 52-week highs suggest institutional capital is genuinely redeploying, not merely parking on the sidelines.

The Philadelphia Semiconductor Index's decline through key moving averages signals that chip stocks may face continued pressure. With the index down over 2% while the broader market rallied, relative strength has definitively shifted away from the group that led markets since 2023.

Investment Implications

This rotation presents both danger and opportunity. Investors overweight in AI-adjacent names face the uncomfortable reality that even companies beating earnings can see double-digit declines if guidance disappoints. The margin for error has vanished.

Conversely, value-oriented sectors that had lagged the AI boom now offer asymmetric upside. Healthcare's combination of defensive characteristics and AI adoption potential makes it particularly compelling—companies that can demonstrate quality business models while participating in the AI revolution may be the true winners of the next phase.

The market is sending a clear message: growth at any price is no longer acceptable. As we enter a period where profitability, balance sheet strength, and cash generation regain importance, the rotation from tech to traditional industry may only be beginning. The AI revolution is real, but the market has finally started asking the right question—at what price?