Summary

-

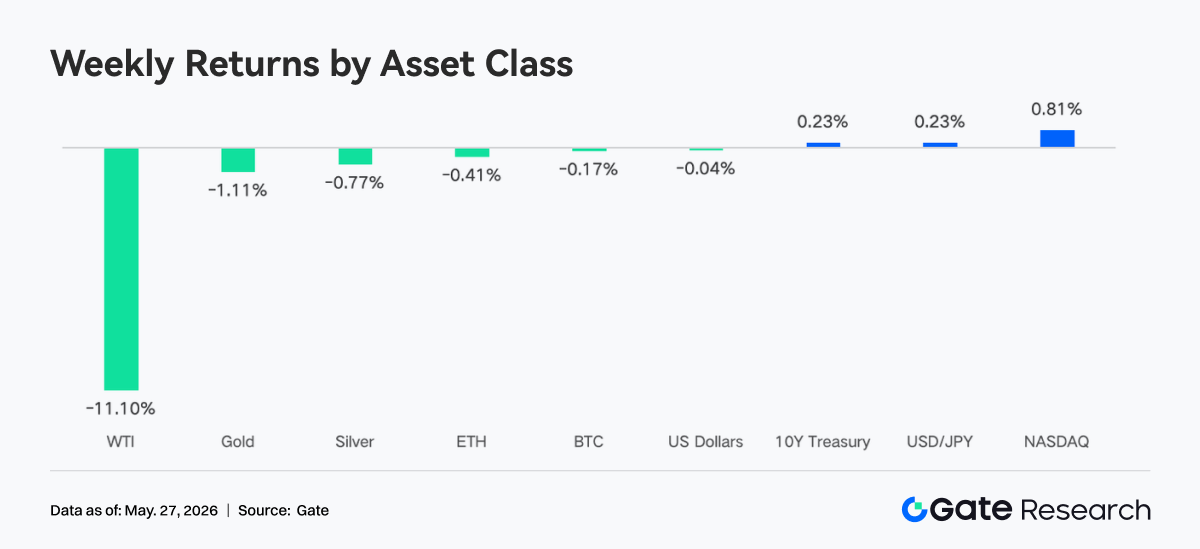

Last week, the market revolved around U.S.-Iran diplomatic negotiations, a surge in U.S. Treasury yields, and the replacement of the Fed chair, with volatility in global risk assets increasing significantly.

-

BTC and ETH recovered after deep pullbacks amid continued ETF net outflows, while overall market sentiment remained cautious.

-

On-chain capital continued to migrate toward execution layers such as Arbitrum and Base, while funding interest in mainnet parking, prediction markets, and macro trading directions cooled noticeably.

-

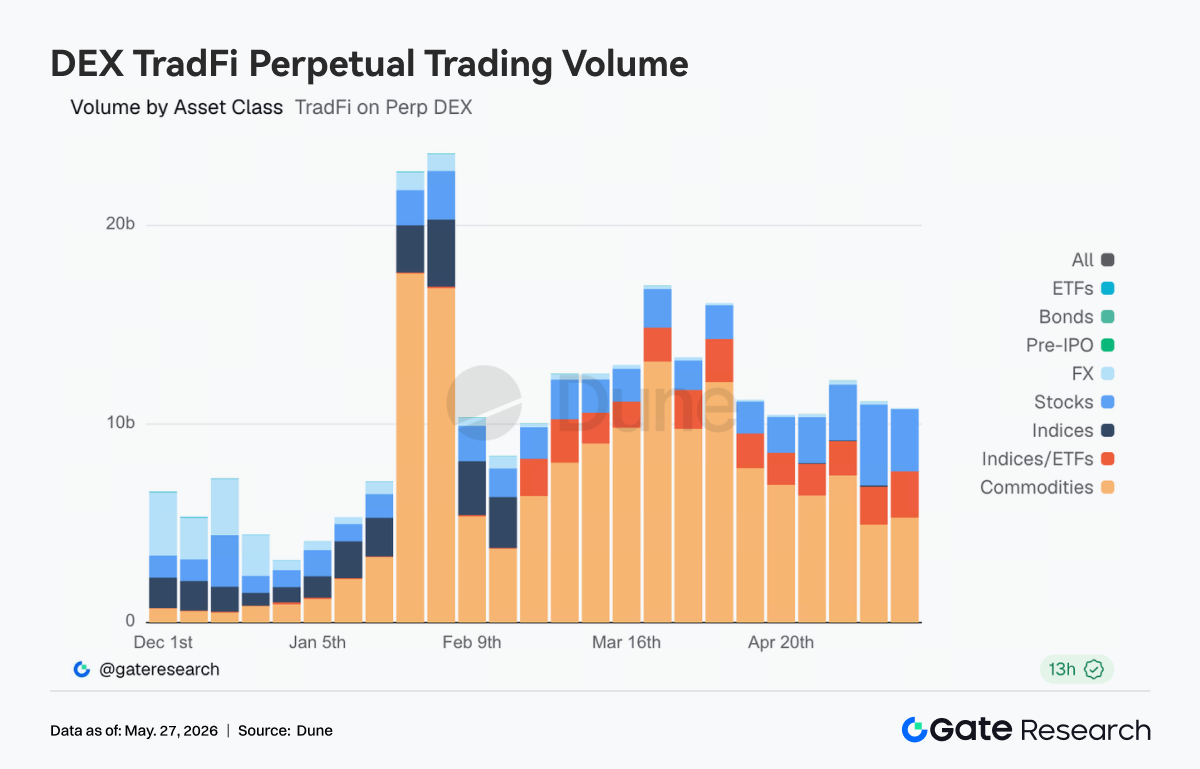

TradFi Perp DEX trading remained centered on gold and crude oil, but activity in equities and AI-related assets began to recover, indicating capital was flowing back into risk assets.

-

Cross-chain infrastructure has suffered nearly $400 million in cumulative losses over the past month-plus. The attack surface has expanded from bridge contracts to validator networks, TSS, and off-chain RPC, prompting the market to reassess cross-chain security risks.

-

The derivatives market showed a “low leverage, low volatility, weak price” structure. Although Skew recovered somewhat, demand for downside protection has not fully faded.

-

Institutional futures and spot market share remained stable. BTC/USDT and ETH/USDT market share rose 5% MoM. CrossEx added spot trading on one major exchange at the end of May.

1. Market Focus Analysis

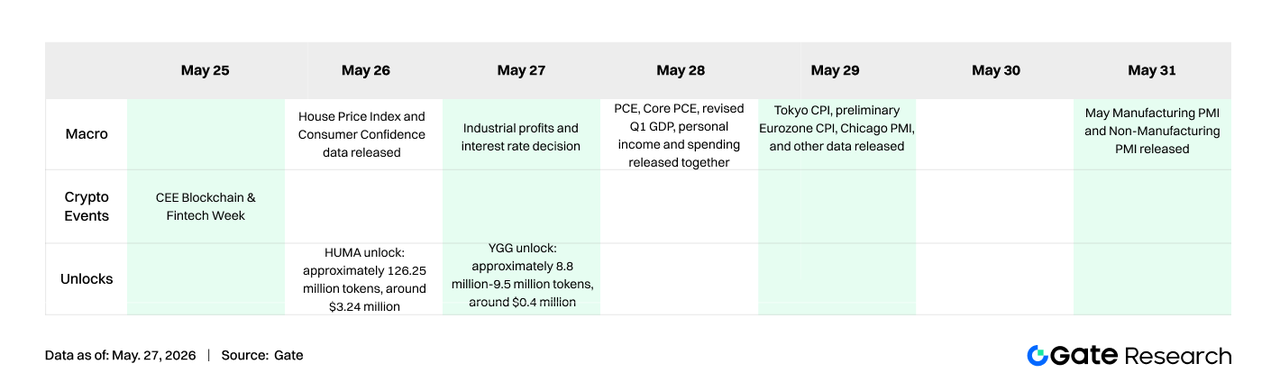

The biggest market theme last week was U.S.-Iran diplomatic negotiations. Trump claimed talks had entered the “final stage,” but Secretary of State Rubio said on Friday that “no agreement has been reached,” with repeated shifts in the geopolitical situation dominating asset price movements. Suppressed by optimism around peace talks, WTI once fell to $98.88 per barrel. Fed Chair Powell’s term ended, and Warsh was officially sworn in as the new Fed chair on May 23. Although he suggested openness to rate cuts, short-term market expectations for cuts have cooled sharply. The 10-year U.S. Treasury yield surged to around 4.56%. U.S. equities rose for an eighth consecutive week, but performance was clearly divergent. Nvidia’s Q1 revenue reached $81.6 billion, up 85% YoY and far exceeding expectations, showing that demand for AI infrastructure remains strong. However, its stock reaction was muted and failed to rise significantly. SpaceX officially filed for an IPO, targeting $75 billion in fundraising and a potential valuation of up to $1.75 trillion.

Last week, crypto market sentiment was generally pessimistic and cautious. Continued net outflows from Bitcoin and Ethereum ETFs reflected investor concerns over macroeconomic uncertainty, crypto price volatility, and the outlook for regulatory policy. In particular, two consecutive weeks of large-scale net outflows from Bitcoin ETFs intensified market panic.

2. Liquidity Analysis

2.1 BTC ETF Scale Continues to Expand

Last week, the BTC ETF market continued to show significant fund outflows. On May 18, it recorded net outflows of $648.60 million, the largest single-day net outflow of the week. Total weekly net outflows reached $1,256.30 million. Compared with the previous week’s $995.50 million in net outflows, the outflow scale expanded further, indicating continued pessimism in market sentiment and ongoing reductions in Bitcoin exposure by institutional investors.

The Ethereum ETF market also faced funding pressure and continued net outflows. On May 18, net outflows reached $86.40 million, the largest single-day net outflow of the week. Weekly net outflows totaled $216.00 million. Compared with the previous week’s $255.20 million in net outflows, the scale narrowed somewhat, but the market remained in an overall outflow state, indicating cautious sentiment toward Ethereum ETFs as well.

-

BTC ETF product with the highest net flow:

- MSBT, Morgan Stanley: weekly net inflow of $1.10 million

-

ETH ETF products with the highest net flows:

-

ETHB, BlackRock: weekly net inflow of $5.50 million

-

ETHW, Bitwise: weekly net inflow of $2.90 million

-

Overall AUM: As of May 22, BTC ETF AUM stood at $98.87 billion, while Ethereum ETF AUM stood at $13.45 billion. The BTC ETF market saw more than $1.2 billion in net outflows, causing total AUM to decline, though it remained at a relatively high level.

-

Institutional trends: Institutional fund flows diverged significantly this week. For Bitcoin ETFs, most products continued to face outflow pressure, with BlackRock’s IBIT seeing net outflows of more than $1 billion, indicating reduced exposure by large institutions. However, Morgan Stanley’s MSBT recorded a small net inflow against the trend, suggesting that some institutions may be conducting tactical allocations or risk hedging. For Ethereum ETFs, BlackRock’s ETHB and Bitwise’s ETHW achieved small net inflows, possibly related to market expectations around Ethereum’s future development or potential positive catalysts, though the overall market remained dominated by outflows.

2.2 TradFi Liquidity

- TradFi Perp DEX: Over the past week, trading activity for TradFi assets on Perp DEXs remained high overall, but the structure showed clear divergence. Commodity assets continued to dominate absolutely, with crude oil and gold-related trading contributing the bulk of volume. However, as U.S.-Iran negotiations eased and oil prices pulled back, commodity trading volume cooled from previous highs. At the same time, the share of equity and index trading increased, reflecting that market capital was beginning to flow back from macro and geopolitical trades into U.S. equities and AI themes. ETF and FX trading remained relatively stable, indicating that on-chain TradFi trading demand is gradually shifting from single-event-driven activity toward a more balanced multi-asset allocation structure.

-

Gate TradFi Perp: Over the past week, Gate TradFi Perp trading volume remained active overall, but cooled noticeably from the March peak. Structurally, precious metals continued to dominate, with gold-related trading contributing the main volume. This reflected continued strong safe-haven demand amid rapidly rising global bond yields and repeated geopolitical uncertainty. However, after entering this week, daily volume fell significantly from prior interim peaks, indicating that the previous high-frequency trading activity around gold, crude oil, and macro events was declining. Meanwhile, the share of equity trading recovered, especially in AI and technology-related assets, showing that some capital was beginning to rotate from macro safe-haven trades back into risk assets. Index, FX, and commodity trading remained low and stable overall, indicating that current on-chain TradFi trading is still centered on gold, but the market structure is gradually shifting from “event-driven” toward more balanced multi-asset allocation.

-

TradFi order book depth: We selected XAUT, the TradFi asset with the highest trading volume, and analyzed its order book depth, Delta. Last week, XAUT’s order book liquidity structure underwent a shift from “short first, long later.” In the early stage on May 13, an extreme negative Delta appeared, with the low close to -$2.2 million, showing that market liquidity was clearly skewed bearish. This coincided with XAUT’s rapid drop from around $4.70K to near $4.60K, indicating strong early selling pressure and liquidity withdrawal. From May 15 to 17, Delta turned clearly positive and remained in the +$500,000 to +$1.3 million range. This meant bids began to rebuild, with a clear bid wall appearing in the order book. However, price did not rebound strongly at the same time, suggesting that the liquidity was more “absorptive liquidity” rather than active momentum buying. Notably, on the 24th and 25th, a clear recovery appeared, with green Delta bars rapidly expanding again and price rebounding back above $4.55K. However, active buy volume was still insufficient to push XAUT into a strong uptrend.

3. On-Chain Data Insights

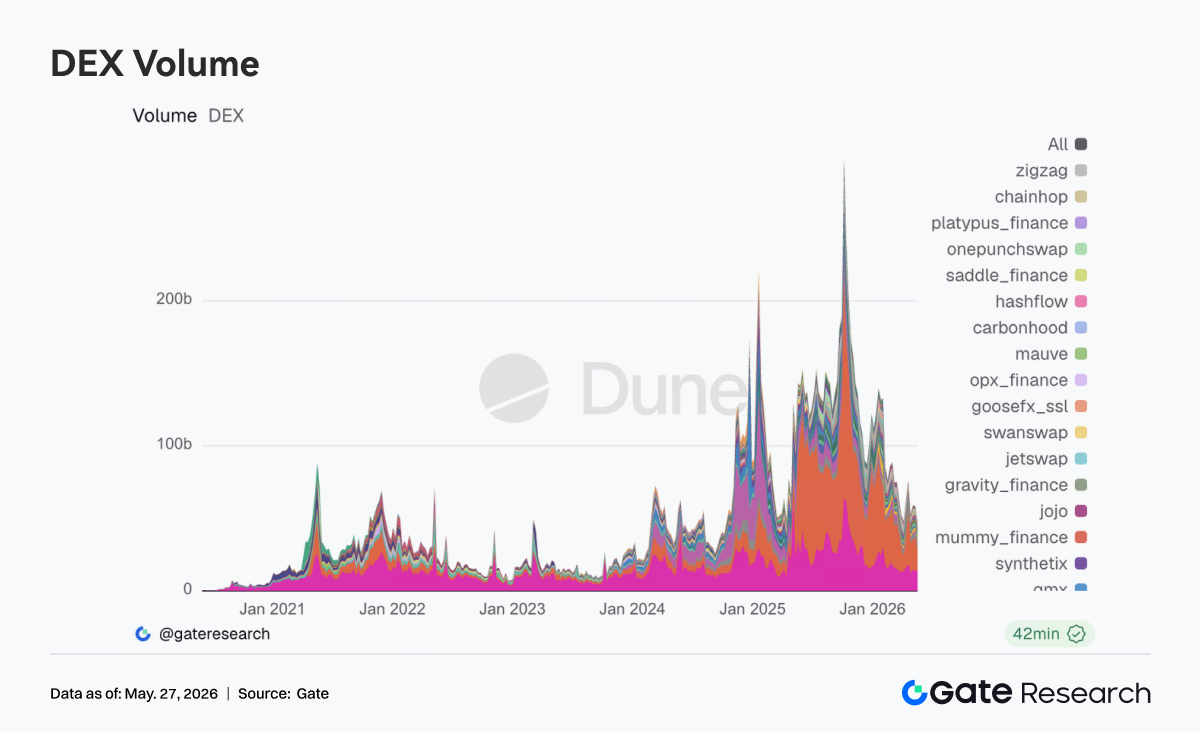

3.1 DEX Trading Remained Resilient, with Volume Concentrating in Mainstream Liquidity Centers

This week, on-chain trading remained highly resilient despite the overall cooling of risk assets. After May 18, Bitcoin once fell to a two-week low, but DEX volume did not lose momentum at the same pace. Instead, capital further concentrated in mainstream protocols with deeper liquidity and more stable execution efficiency. Uniswap and PancakeSwap continued to occupy core trading shares, while activity in Aerodrome within the Base ecosystem increased further. On-chain trading demand did not withdraw; rather, in a volatile environment, it showed a preference for mature routing and low-slippage platforms.

On the Solana side, Raydium and Meteora remained at high levels, but marginal growth slowed noticeably compared with previous weeks. Interest in meme assets and high-volatility liquidity pools began to cool. On the regulatory front, after the Senate Banking Committee advanced crypto market-related legislation in mid-May, market valuations for compliant trading infrastructure rose, and on-chain liquidity further concentrated in leading protocols.

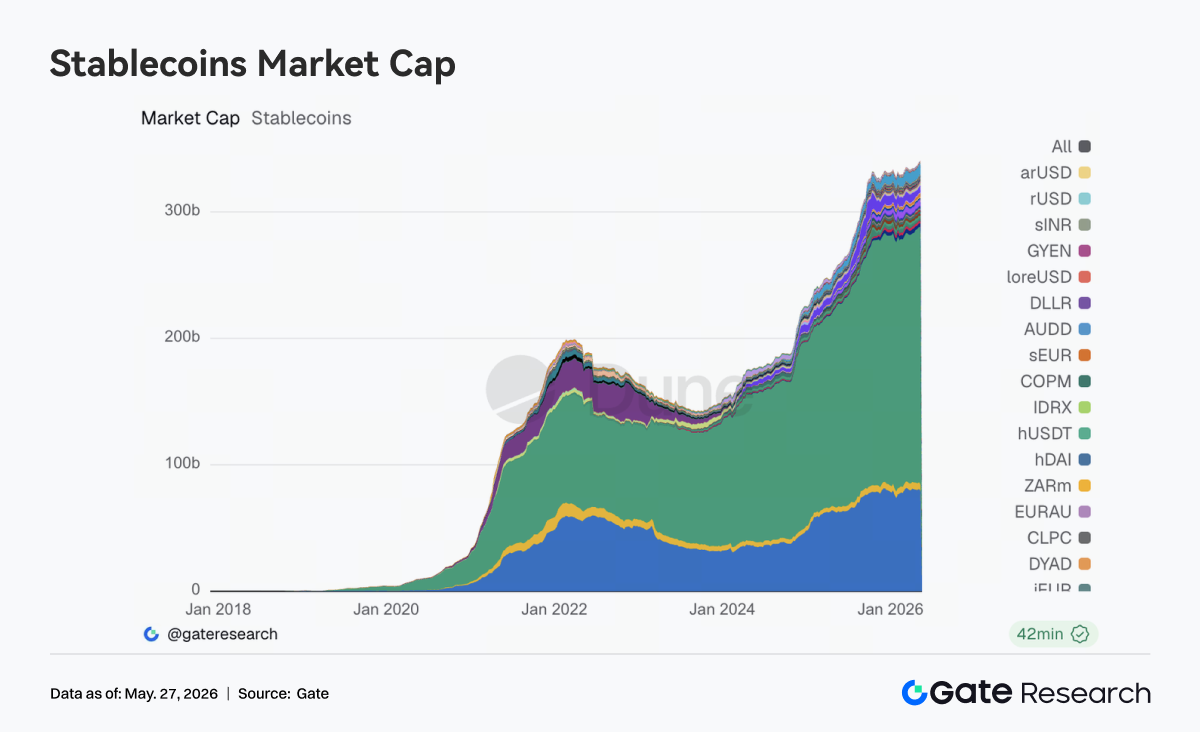

3.2 Stablecoin Market Entered a Structural Repricing Phase, with Settlement Capacity and Institutional Compatibility Becoming Core Variables

This week, the stablecoin sector did not see rapid expansion at the aggregate level, but internal structural adjustments continued to deepen. USDT and USDC remained dominant, but the focus of new capital has gradually shifted from simple scale growth toward payments, clearing, cross-chain distribution, and institutional compatibility. Assets such as USDS, USDe, and PYUSD still showed some absorption capacity, but the market’s distinction between “yield-bearing stablecoins” and “general-purpose dollar settlement assets” became more pronounced.

This week, Circle continued to strengthen USDC’s positioning in cross-chain settlement, high-frequency trading, and institutional distribution scenarios. The market also refocused on stablecoin assets that can directly connect to mainstream financial systems. At the same time, regulatory discussions around stablecoin yield mechanisms and regulatory boundaries continued to advance. The stablecoin market’s valuation logic is gradually shifting from scale-first to compliance standardization capability-first. Overall, sentiment in the stablecoin sector was stable this week, but the direction was relatively clear.

3.3 ETH LST Assets Came Under Pressure, While SOL Assets Remained Relatively Stable

The liquid staking sector entered a more obvious phase of structural divergence. Core ETH-based assets such as Lido saw some pullback, as some large funds readjusted positions and duration allocation after the earlier recovery. By contrast, SOL-side assets were more resilient, with Sanctum, Jito, and Jupiter Staked SOL remaining broadly stable and the sector seeing no obvious outflow pressure.

The core variables affecting LST risk appetite this week still came from cross-chain security and asset standardization. In mid-May, Lido further explained its reasons for choosing Chainlink CCIP for wstETH cross-chain expansion, and the market renewed its focus on bridge security and standardized asset frameworks. After the Kelp and cross-chain bridge incidents, the market has gradually begun to differentiate risk levels between native standardized LSTs and secondarily wrapped bridged assets.

3.4 Aave Lending Demand Continued to Migrate, with New Markets Improving Absorption Capacity

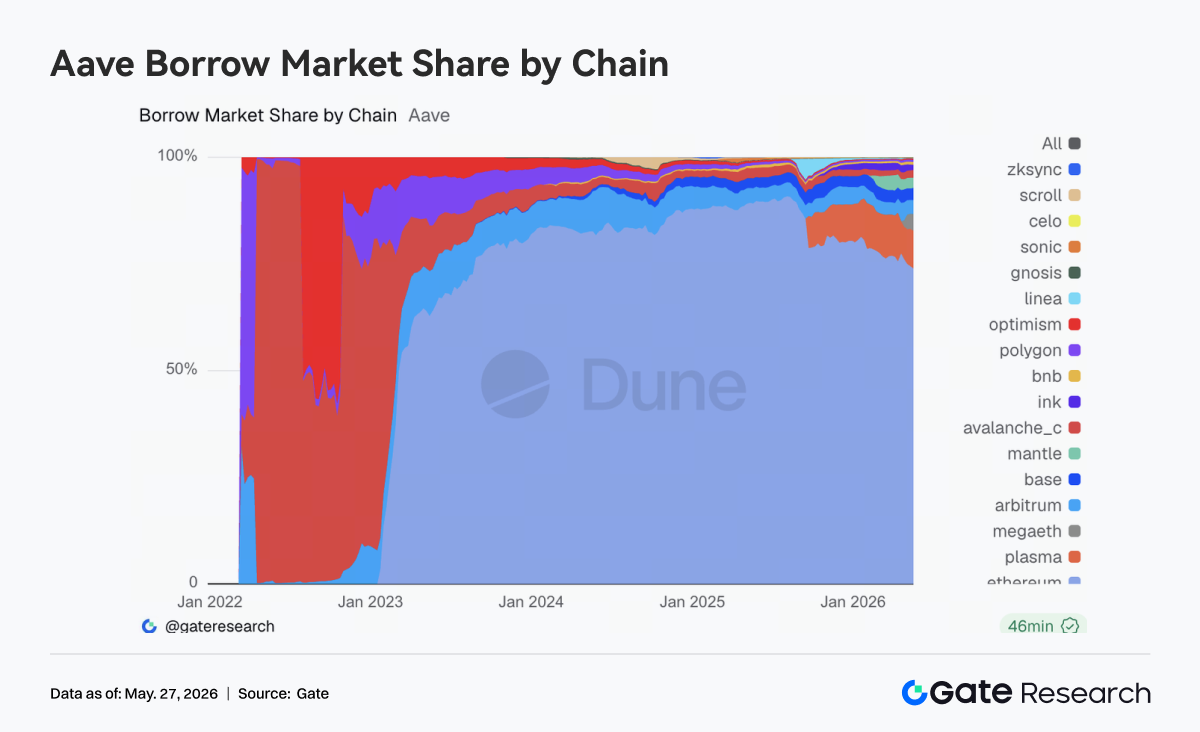

The main change in Aave this week centered on adjustments in the lending demand structure. Total borrowing across the platform fell somewhat from last week. Ethereum V3 still maintained its core position, but its marginal pull was weaker than in previous phases. Meanwhile, the lending absorption capacity of Plasma and MegaETH continued to strengthen. MegaETH was particularly notable, with both capital retention time and activity improving significantly, gradually shifting from narrative-driven demand to real liquidity absorption.

On the governance side, Aave advanced Emergency Guardian signer rotation on May 20, raising emergency response and cross-chain risk control to a higher priority. Previous governance actions around WETH unfreezing and LTV restoration also showed that the protocol has gradually moved from the risk disposal phase after the rsETH/Kelp chain reaction to a normalized rebuilding phase. From the current structure, capital is flowing back into the Aave ecosystem, but it is more inclined toward on-chain scenarios with new incentives and new market growth space.

3.5 Aave Interest Rate Structure Normalized, While the Dollar Liquidity Premium Remained Clear

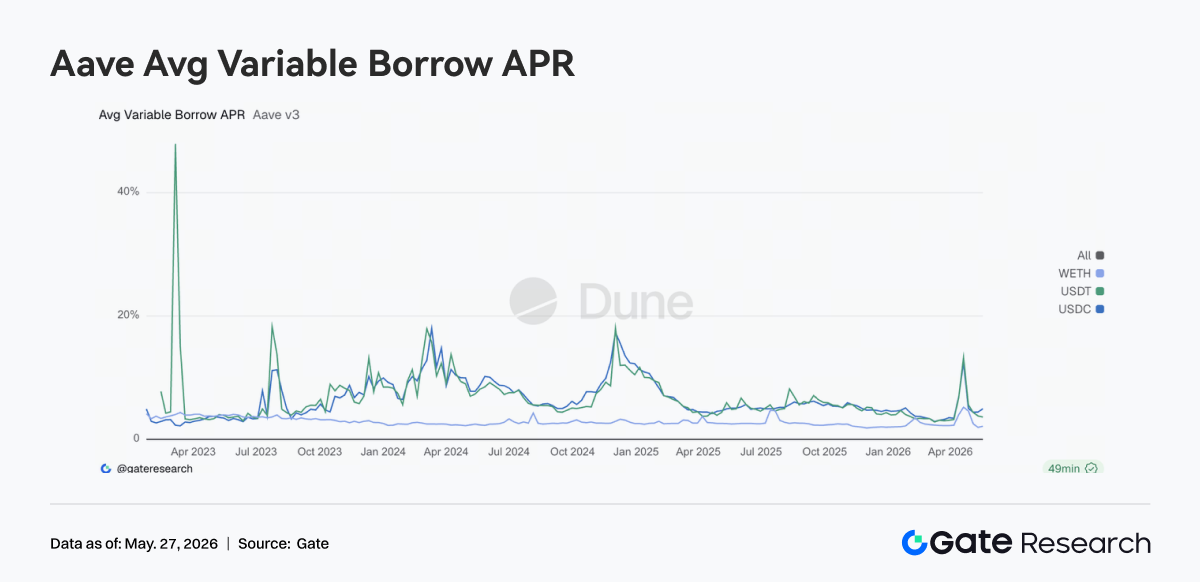

Aave stablecoin borrowing costs have clearly moved away from the high-pressure state seen during the late-April event period. USDT and USDC funding rates fell back to a normal operable range, while WETH borrowing costs declined further. The core market change is that capital usage has returned to a normal structure. Stablecoin financing demand is mainly concentrated in arbitrage, neutral strategies, and liquidity turnover, while the WETH side has not seen a new wave of one-sided borrowing demand.

However, USDC utilization remains relatively high, and dollar liquidity is still the most premium funding category in the market. Overall, though, the financing environment has clearly weakened the tension seen during the previous risk event period. Combined with this week’s further governance strengthening of emergency mechanisms and the Guardian framework, the current change in Aave rates represents a normalized repricing process after risk release.

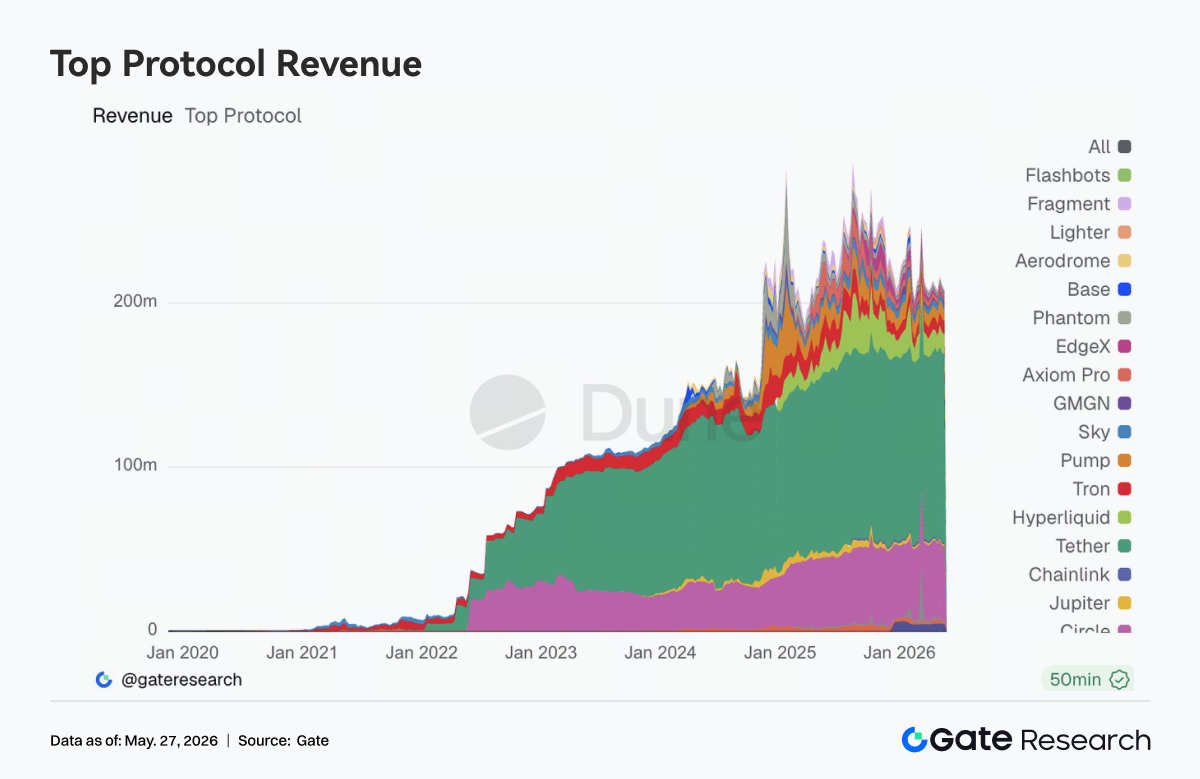

3.6 Protocol Revenue Returned to a Stablecoin- and Infrastructure-Led Structure

The protocol revenue structure became noticeably more stable compared with previous weeks. Tether and Circle continued to maintain the most stable revenue performance, and stablecoin issuance remains the core sector with the highest-quality on-chain cash flow. Among trading protocols, Hyperliquid revenue remained high, but growth slowed noticeably. Revenue from protocols driven by trading entry points and high-frequency traffic, such as Pump, Phantom, and Axiom, also began to cool.

By contrast, underlying matching and infrastructure layers such as edgeX and Titan Builder showed stronger resilience. Recently, Hyperliquid has continued to advance expansion directions including validators, RWA perpetuals, and event markets. Circle has also strengthened USDC support for Hyperliquid, showing that long-term market demand for efficient on-chain trading systems has not weakened. However, this week’s revenue structure shows that user activity expansion is no longer spilling over without limit. Capital has begun to refocus on underlying settlement, matching, and clearing layers with sustainable cash-flow retention capacity. Overall, protocol revenue logic is gradually returning to cash-flow quality.

4. Derivatives Tracking

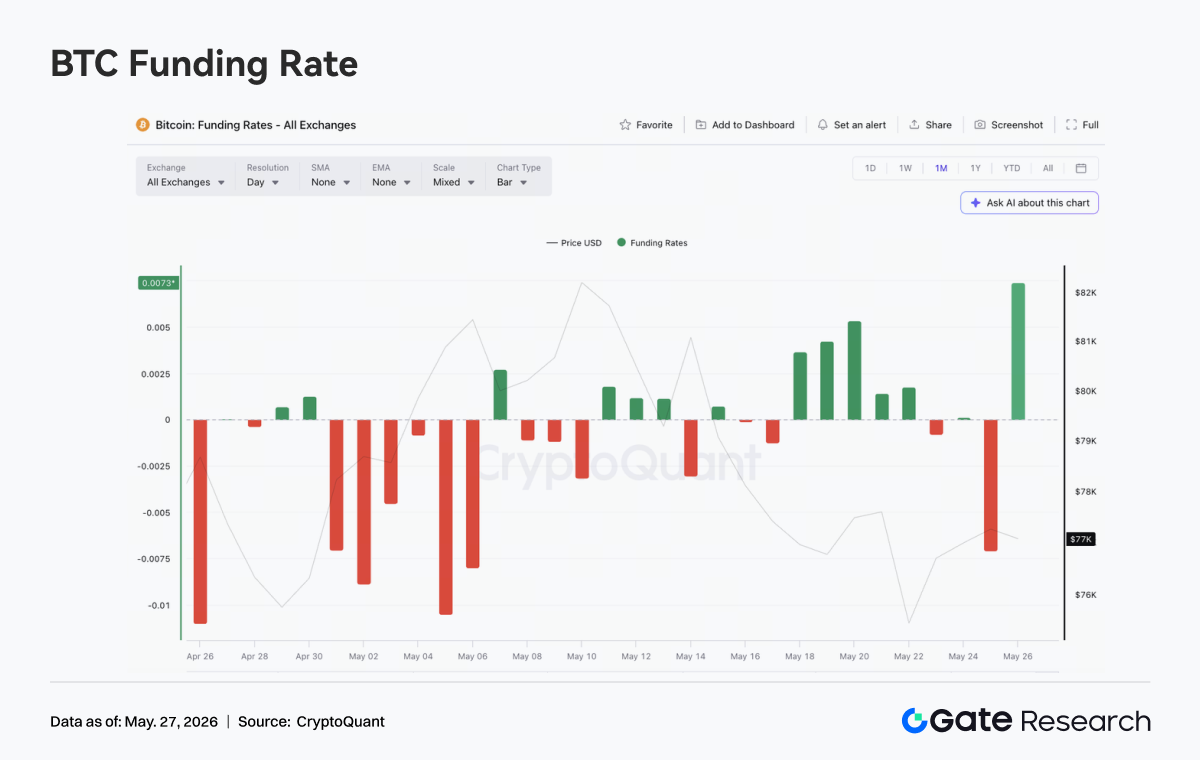

4.1 BTC Funding Rates Remained Positive but Price Was Weak, Pressuring Leveraged Longs

From May 18 to May 24, 2026, BTC price remained broadly weak and range-bound. It traded near 77K at the start of the week, and although there were intermittent rebounds, it failed to effectively reclaim the 78K-79K range. Around May 22, price briefly dropped quickly and remained relatively low over the weekend.

Diverging from price performance, funding rates remained positive multiple times from May 18 to May 22. In particular, positive funding continued to rise from May 18 to May 20, indicating that some longs maintained leveraged exposure despite weak prices.

This combination of “weak price + positive funding” reflects that the market still had some dip-buying or rebound-trading expectations at the beginning of the week. But as BTC failed to recover upward, long positions in a positive funding environment continued to bear costs, and funding rates later gradually fell, showing that long sentiment began to cool.

In terms of OI, this week it generally fluctuated in the $25 billion-$26 billion range, clearly below the previous high near $29 billion. When price dropped quickly on May 22, OI briefly rebounded to around $26 billion, suggesting that new directional positions entered during the decline. However, OI then fell again, indicating that leveraged capital did not continue adding positions. Overall, this week’s derivatives market was in a low-leverage consolidation state, with the price decline reflecting more of a fall in risk appetite than a large-scale leveraged liquidation cascade.

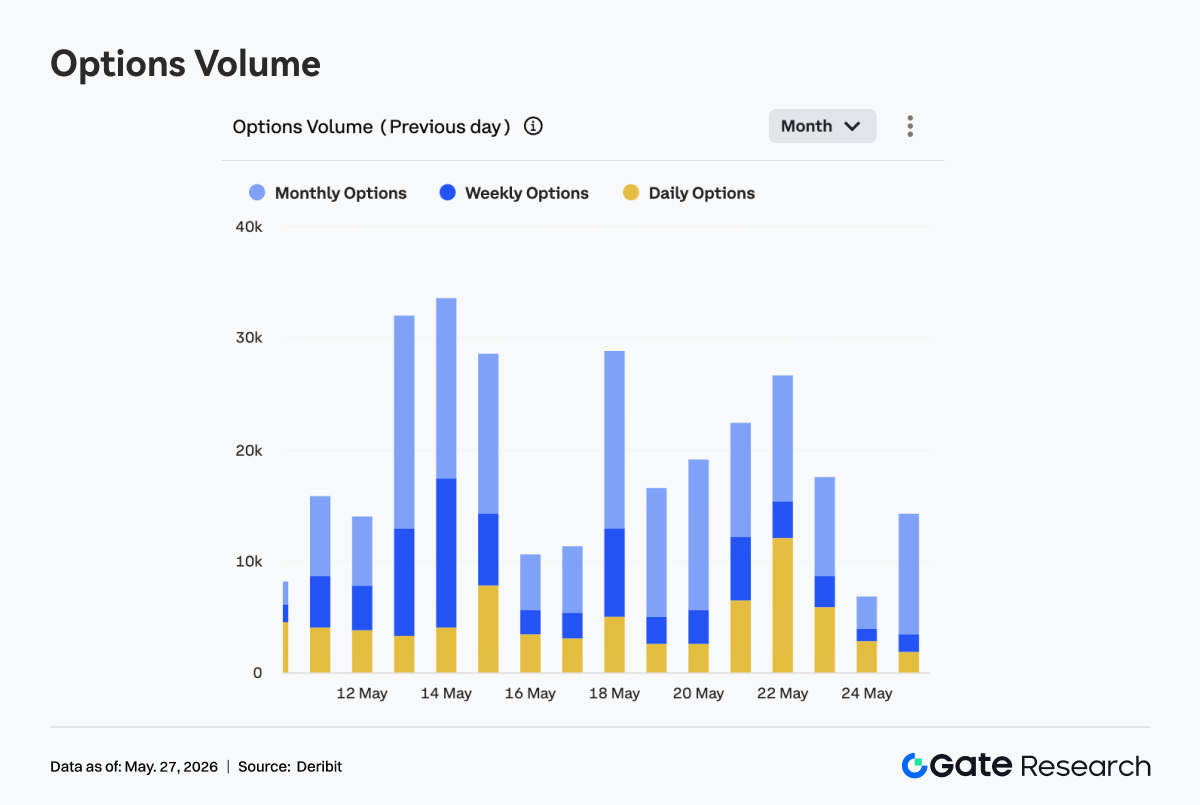

4.2 Options Volume Fell First, Then Rose, While the Rising Share of Daily Options Showed Stronger Short-Term Trading Demand

BTC options volume followed a pattern of first declining, then rising, and later pulling back. On May 18, volume was at a weekly high, close to 29K. It then fell to around 16K-19K from May 19 to May 20, showing that after early-week macro and price volatility was absorbed, market trading activity cooled temporarily. From May 21 to May 22, volume expanded again. On May 22, it rose to around 26K, the second obvious peak of the week, corresponding to BTC’s rapid price drop. This showed that hedging and short-term volatility trading demand rose simultaneously during the decline.

Structurally, monthly options remained the main source of volume, especially around May 18 and May 20, indicating that the market was still mainly focused on medium-term allocation and risk management. But the more notable point this week was the clear rise in the share of daily options. From May 21 to May 23, the yellow portion expanded significantly, especially on May 22, when daily options contributed a large share of volume. This shows that when prices fell and short-term volatility intensified, the market preferred to use short-dated tools for event trading or rapid hedging.

Overall, the options market this week did not see sustained one-sided volume expansion, but rather pulse-like volume increases during the price decline. The structure dominated by monthly options shows that medium-term positions have not exited, while the rising share of daily options reflects stronger short-term risk management demand. Combined with Skew remaining negative and DVOL trending lower overall, the market did not enter full panic pricing, but sensitivity to downside protection and short-term volatility trading increased noticeably on key price volatility days.

4.3 25D Skew Recovered from Deep Negative Levels, but Downside Protection Premium Did Not Disappear

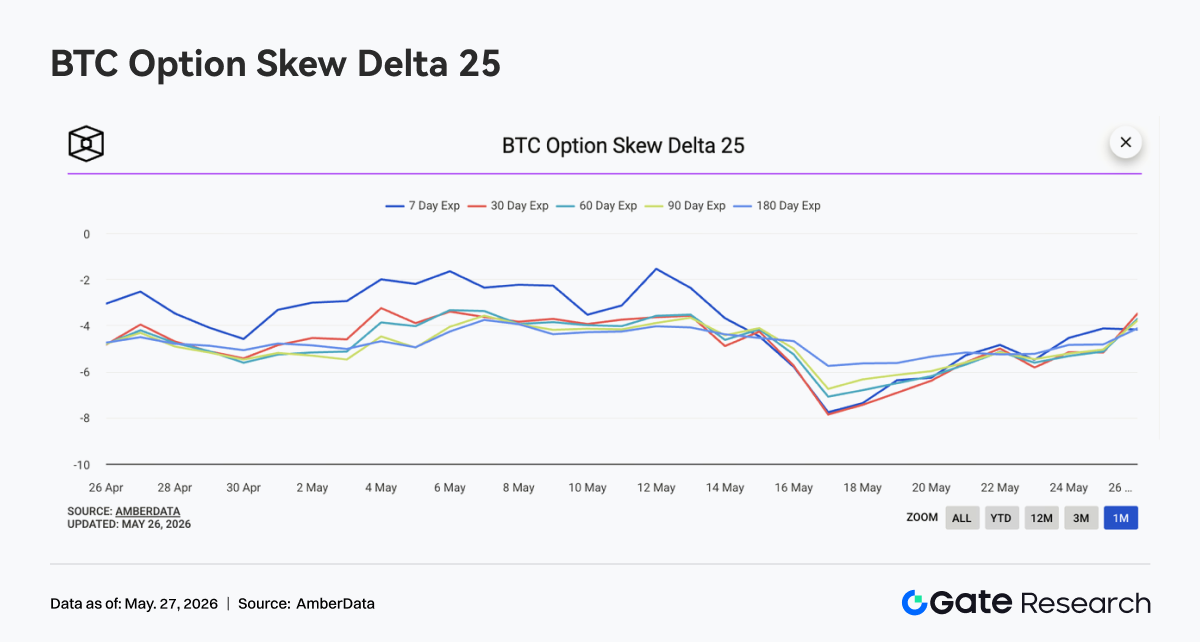

BTC 25D Skew across maturities gradually recovered from deeply negative territory. At the start of the week, 7D and 30D Skew once approached -8, showing that after the previous week’s price decline, demand for short-term downside protection was very strong. As price then entered low-level consolidation, Skew across maturities began to rebound. By around May 24, short-term Skew had recovered to around -4.5, while medium- and long-term maturities also rose.

The recovery in Skew shows that panic-driven protection demand eased somewhat, and short-term put premiums fell noticeably from the beginning of the week. However, it should be noted that Skew across maturities remained negative overall, meaning the market has not fully shifted optimistic, and options pricing still retains a defensive stance toward downside risk.

Overall, this week’s Skew changes reflect the market’s shift from “concentrated protection buying” to “low-level wait-and-see.” If BTC continues to trade sideways, Skew may recover further. But if price breaks below the previous low again, short-term Skew may weaken rapidly once more.

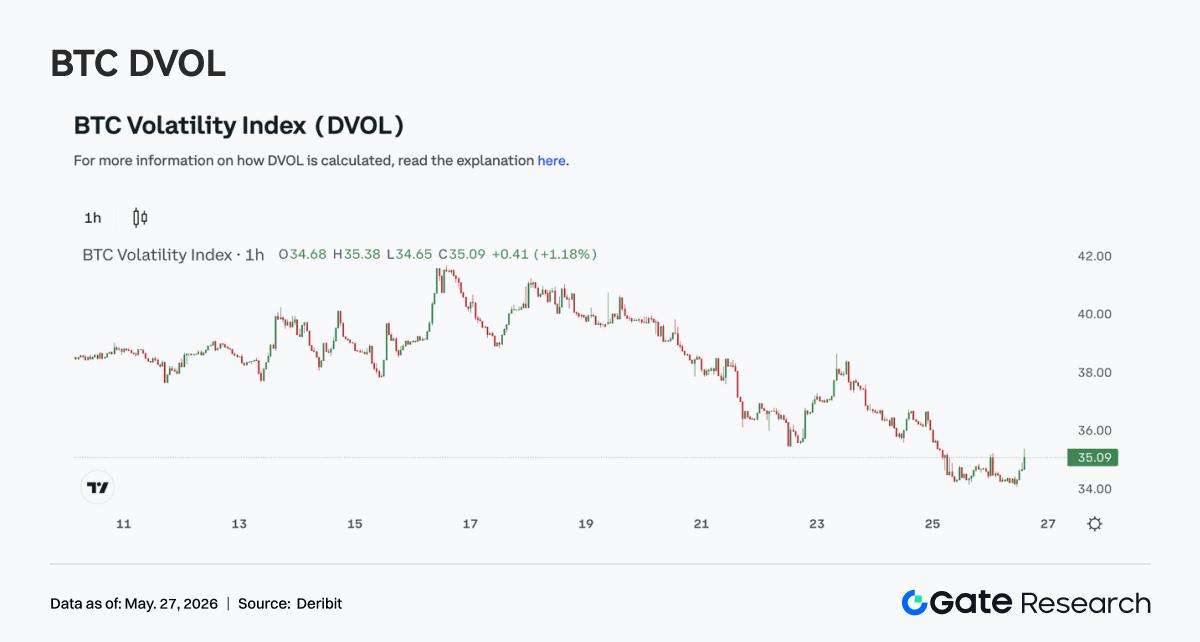

4.4 DVOL Continued to Decline, with Volatility Compressing Despite Weak Prices

This week, the BTC volatility index DVOL showed an overall choppy downward trend. At the start of the week, DVOL remained near 40, then gradually fell. Although there was a brief disturbance when price dropped on May 22, DVOL failed to rise again meaningfully, and by May 24 it had fallen to around 36.

Weak price action combined with declining DVOL shows that the market’s reaction to the decline did not appear as panic-driven volatility expansion. Instead, it was closer to a “slow de-risking + volatility decline” structure. This is consistent with low OI consolidation and Skew recovery, indicating that after the earlier risk release, both leverage and protection demand cooled.

Overall, BTC derivatives this week showed a combination of low leverage, low volatility, and weak price. In the short term, the market lacks a clear directional catalyst. If price continues to consolidate at low levels, DVOL may remain low. However, because Skew is still negative, if price breaks below key support again, volatility still has room to expand again.

5. Outlook

6. Gate Institutional Updates

Institutional Business Growth

-

Institutional futures and spot market share remained stable.

-

BTC/USDT and ETH/USDT market share rose 5% MoM.

-

Multiple global quant, high-frequency, and asset management institutions entered the integration and testing phase.

Institutional Lending Upgrade

-

The new 0 lending solution was officially launched, further lowering the lending threshold and raising the single-client borrowing cap to 10 million USDT.

-

A new discount campaign for fixed-term collateralized borrowing will launch soon.

CrossEx Development

Continued Technical Infrastructure Optimization

-

Continued optimization of WebSocket latency and order push issues.

-

Spot SBE, OMS 3.0, and CrossEx upgrades continued to advance.

Brand and Global Events

The June 2 Institutional event in Amsterdam continued to progress, and the second round of invitations to global institutional clients has begun.

Data Sources

-

Investing, https://investing.com/currencies/xau-usd-historical-data

-

Gate, https://www.gate.com/trade/BTC_USDT

-

CMC, https://coinmarketcap.com/real-world-assets/?type=all-tokens

-

Coinglass, https://www.coinglass.com/pro/depth-delta

-

Dune, https://dune.com/gateresearch/gate-tradfi#weekly-volume

-

Dune, https://dune.com/gateresearch/gate-institutional-weekly-report

-

Bybit, https://www.bybit.com/future-activity/en/tradfi

-

Bitget, https://www.bitgettradfi.com/tradfi/XAUUSD

-

CryptoQuant, https://cryptoquant.com/asset/btc/chart/derivatives

-

Amberdata, https://pro.amberdata.io/options/deribit/btc/current/

Gate Research is a comprehensive blockchain and cryptocurrency research platform that provides deep content for readers, including technical analysis, market insights, industry research, trend forecasting, and macroeconomic policy analysis.

Disclaimer

Investing in cryptocurrency markets involves high risk. Users are advised to conduct their own research and fully understand the nature of the assets and products before making any investment decisions. Gate is not responsible for any losses or damages arising from such decisions.