AAVE V4 Officially Launches: Why This Upgrade Deserves Attention

Image source: AAVE Official Post

Image source: AAVE Official Post

The mainnet debut of AAVE V4 stands out as one of the most pivotal protocol upgrades in DeFi for 2026. This significance isn’t merely due to Aave’s scale or market share. Instead, V4 directly tackles the most critical bottlenecks facing DeFi lending as it enters its next phase: fragmented liquidity within a single chain, insufficient risk management granularity, limited support for emerging asset types, and the challenges of integrating institutional and RWA use cases.

Aave has confirmed that V4 is now live on the Ethereum mainnet. Coupled with previous statements that “V4 will launch on mainnet in 2026,” it’s clear that Aave has transitioned from testnet to full mainnet activation. For the industry, this marks a shift: Aave is moving beyond incremental pool optimization, aiming to evolve DeFi lending into a universal credit layer capable of supporting more asset types, diverse risk models, and expanded business scenarios.

Aave V4 Mainnet Launch: Timeline, Scope, and Initial Configuration

According to the official Aave blog, V4 went live on the Ethereum mainnet in March 2026. This was not an “all-at-once, aggressive expansion,” but a security-first, phased rollout.

Three core elements define this launch:

-

V4 is now operational on Ethereum mainnet, with user interactions available via the Aave Pro interface.

-

The initial deployment features three primary Liquidity Hubs: Core Hub, Prime Hub, and Plus Hub.

-

All Hubs and Spokes launched with relatively conservative supply and borrow caps. The Aave DAO will gradually adjust these limits based on on-chain activity.

This approach reflects Aave’s measured stance toward V4. Despite the scale of the architectural upgrade, the DAO chose not to immediately expand risk exposure with the “official launch.” Instead, the protocol will first be tested in real production environments for liquidity routing, risk management, and governance response—a strategy consistent with Aave’s historical approach to major upgrades.

What’s Changed from AAVE V3 to V4

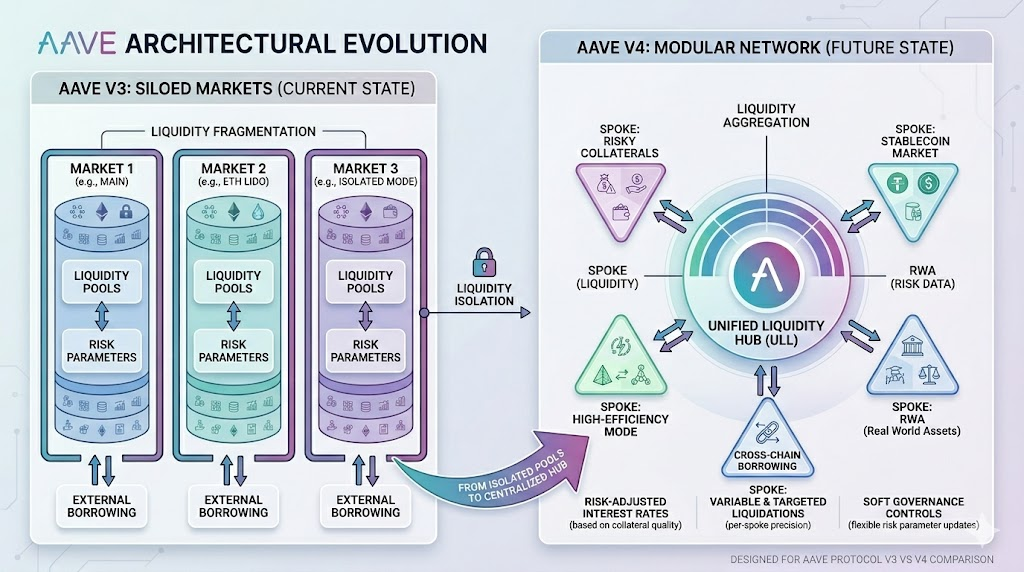

The most significant change from AAVE V3 to V4 isn’t just new features—it’s the transformation of “markets” into a “liquidity hub plus functional spoke” architecture.

The most significant change from AAVE V3 to V4 isn’t just new features—it’s the transformation of “markets” into a “liquidity hub plus functional spoke” architecture.

In V3, different instances or markets on the same chain operated with independent liquidity. When users deposited assets into a market, those assets could only be lent within that market. This ensured clear structure and isolation, but resulted in fragmented liquidity. Even well-designed new markets had to attract deposits from scratch, limiting capital efficiency.

V4 replaces this with a Hub and Spoke architecture. The Hub centralizes liquidity and unified accounting, while Spokes define specific lending scenarios, collateral requirements, risk parameters, and liquidation logic. In effect, V4 separates “liquidity” from “risk expression”: liquidity is unified, risk is segmented.

Beyond architecture, V4 introduces three critical upgrades:

-

Risk premium mechanism. In V3, borrowing rates for the same asset within a market were driven by supply and demand, with collateral risk differences not fully priced in. V4 introduces risk premiums based on collateral quality—high-quality collateral enjoys lower borrowing costs, while high-risk collateral bears higher financing costs.

-

More granular liquidation mechanism. V3 relied on a fixed close factor and relatively static liquidation rewards. V4 brings in a target health factor and variable liquidation rewards, making liquidations more targeted—repairing positions as needed rather than applying blanket liquidations.

-

Dynamic risk configuration. V4 allows governance to apply new risk parameters to new positions without disturbing existing ones, providing flexible governance tools for market changes or asset delisting.

Hub and Spoke Architecture: V4’s Core Innovation

The Hub and Spoke model is the most critical innovation in Aave V4.

The Hub serves as the central liquidity anchor for each chain. Users deposit and borrow assets via Spokes, but underlying liquidity is managed centrally by the Hub. Spokes act as modular interfaces for different user groups, asset types, and risk profiles. They can power stablecoin markets, ETH staking derivatives, isolated asset pools, or future RWA and custodial lending scenarios.

This design directly addresses a persistent V3 issue: isolating risk in new markets required isolating liquidity, which hurt capital efficiency. V4’s approach is to isolate risk at the Spoke level while maintaining liquidity efficiency at the Hub.

This shift brings three advantages for Aave:

-

Launching new niche markets is easier. New Spokes can inherit Hub liquidity without bootstrapping new pools.

-

Risk management is more granular. Each Spoke can have its own collateral, borrowable assets, parameters, and liquidation rules.

-

Protocol scalability is greatly enhanced. Whether for permissioned institutional markets or dedicated RWA structures, deployment within the V4 framework becomes straightforward.

Strategically, this allows Aave to optimize between “unified liquidity” and “differentiated risk markets,” rather than being forced to choose one over the other.

How the Risk Premium Mechanism Reshapes Borrowing Rates

The risk premium upgrade in V4 addresses a fundamental issue in DeFi lending: risk has not been priced with sufficient precision.

In V3, borrowing rates for a given asset were largely set by supply and demand. This meant users could borrow the same asset at similar rates, regardless of whether they posted WETH or a more volatile, illiquid long-tail asset as collateral. This setup resulted in high-quality collateral subsidizing higher-risk collateral.

V4 changes this dynamic. The Hub still provides a base rate, but the final borrowing cost depends on the risk quality of the collateral. Higher-quality collateral incurs lower risk premiums; riskier collateral faces higher premiums.

This delivers several benefits:

- Borrowers see financing costs that reflect collateral quality.

- Depositors and the DAO receive more appropriate returns and fees from higher-risk loans.

- The protocol can support more asset types, as high-risk assets no longer require raising risk costs for the entire market.

Most importantly, this mechanism brings Aave closer to the logic of traditional credit markets, where different risks command different funding prices—a necessary step for protocols targeting institutional and RWA markets.

Why the New Liquidation Engine Is More Granular and Efficient

Liquidation mechanisms are the core safety valves of lending protocols. Aave has processed nearly 295,000 liquidations totaling more than $3.3 billion. For a protocol of this scale, liquidation precision directly impacts user experience, bad debt management, and system stability.

While V3’s liquidation mechanism has proven reliable, it had a clear drawback: liquidations were executed at a fixed ratio, often resulting in excessive repayment of debt and collateral for mildly risky positions.

V4 overhauls this with a new liquidation engine. Rather than fixed-ratio liquidations, V4 uses a governance-set target health factor to calculate the maximum debt needed to restore a position’s safety. This enables precise, targeted liquidations.

V4 also introduces variable liquidation rewards—the lower the health factor, the higher the reward. This incentivizes liquidators to quickly address the riskiest positions, improving protocol resilience during volatility.

For users, this means less risk of “over-liquidation” for mildly risky positions. For the protocol, liquidation incentives align more closely with actual risk.

What V4 Means for RWA, Institutional Markets, and New Asset Support

V4 is more than a “next-generation lending pool”—its strategic value is broader.

Aave’s 2025 review and V4 documentation highlight a key goal: supporting more complex assets and participant structures beyond crypto-native collateral. This includes RWA, permissioned lending, borrowing through qualified custodians, and integration with broker and margin accounts.

In V3, these needs were met by creating independent markets—ensuring isolation but limiting liquidity and composability. V4 enables a new approach: custom Spokes can set special rules, access requirements, liquidation parameters, and collateral logic, while the Hub pools underlying liquidity.

This positions Aave as more than the largest DeFi lending protocol—it becomes an on-chain credit framework, open to diverse asset classes, regulatory regimes, and user types. If V4 operates stably, the upgrade expands Aave’s boundaries beyond just TVL growth.

Opportunities, Constraints, and Key Observations After AAVE V4 Mainnet Launch

On the opportunity side, AAVE V4 brings three major enhancements: higher same-chain liquidity utilization, more precise risk pricing, and greater modular market expansion. These upgrades strengthen Aave’s competitive advantage in DeFi lending and may boost its appeal to institutional and RWA partners.

However, there are challenges:

- V4 is a major architectural overhaul. Despite 345 days of security reviews by multiple audit firms, independent researchers, and public competitions, audits do not guarantee the absence of new production risks.

- The Hub and Spoke model increases flexibility but also system complexity, making governance, monitoring, parameter management, and emergency response even more critical.

- Whether V4 can truly deliver “unified liquidity without amplifying systemic risk” depends on sustained mainnet performance, including the quality of new Spokes, adjustment of caps, liquidation efficiency, and real user adoption.

At this stage, the most objective assessment is that AAVE V4 has crossed the launch threshold, but its true value remains to be proven.

Conclusion

The AAVE V4 mainnet launch is more than just a version upgrade—it’s a systemic answer to the evolution of DeFi lending infrastructure. V3 solved “multi-chain expansion and basic risk isolation.” V4’s challenge is “how to maintain liquidity efficiency, risk control, and scenario expansion in a more complex asset world.”

Viewed in this light, V4 is far more than a routine upgrade. It aims to transform Aave from a leading lending protocol into a true on-chain credit operating system. For the market, this is both a key growth signal and an ongoing governance experiment. Over the coming quarters, how the Aave DAO raises Hub and Spoke caps, launches specialized Spokes, and how V4 performs amid real on-chain volatility will determine whether this launch is a technical milestone or the start of the next DeFi credit expansion wave.