According to CryptoRank, only six Initial Coin Offerings (ICOs) were completed in 2026 to date, with half trading below their offering prices. Crypto financing is undergoing a structural shift, with venture capital funding rounds also decelerating in April compared to earlier in the year. The six ICOs utilized established platforms CoinList or Echo rather than independent sales events, reflecting a broader move away from standalone token offerings.

ICO Market Contraction

The ICO market, which dominated fundraising during the 2017 bull market, has been progressively displaced by alternative models. Smaller crypto projects have migrated to airdrops or launched as tokenless applications, while larger companies pursue initial public offerings (IPOs) on traditional stock exchanges. This structural transition underscores diminishing investor appetite for the ICO format.

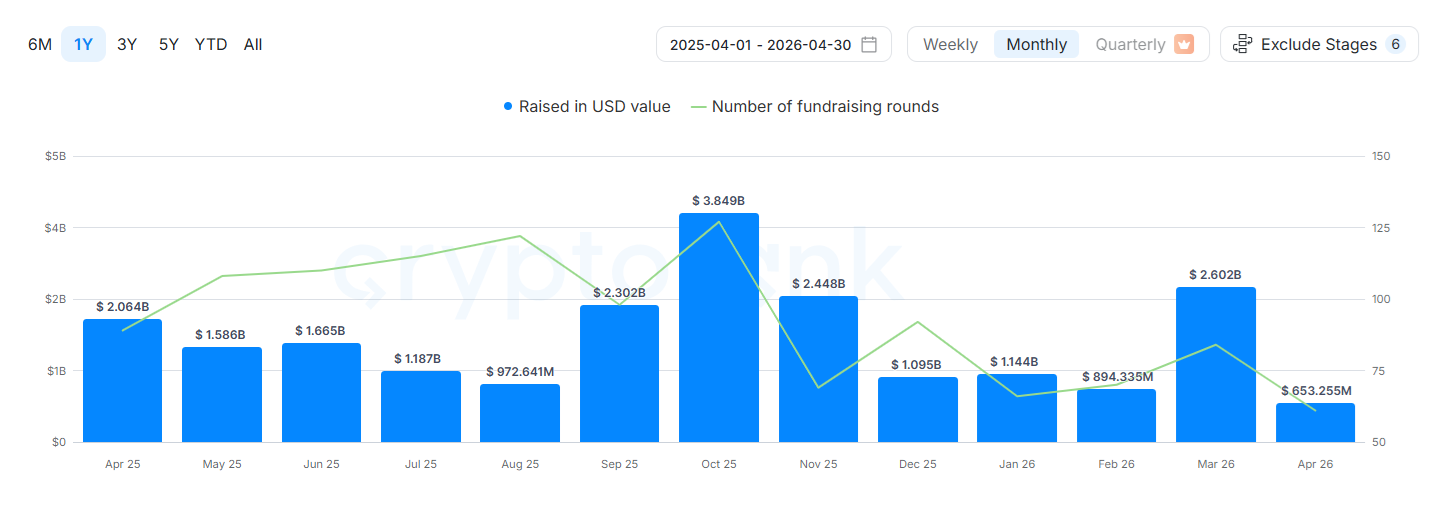

VC Funding Outflows in April

Crypto venture funding experienced a sharp reversal in April 2026. According to CryptoRank data, only $653 million was raised across 61 funding rounds in April—the lowest monthly total in the past 12 months. This contrasts sharply with April 2025, when venture funds raised over $2 billion across 89 funding rounds.

Participant composition also shifted. GSR emerged as the leading investor with four deals in April, including one lead round. Animoca Brands and Coinbase Ventures, which had dominated funding activity in previous months, participated in just three rounds each during April. US-based funding particularly contracted, with only $150 million deployed domestically. The majority of funding rounds ($594 million) occurred in undisclosed jurisdictions, while European investors retreated from early-stage and ongoing crypto project support.

Token Sales and Market Sentiment

Token sales across all formats—including platform-based Initial DEX Offerings (IDO) and Initial Exchange Offerings (IEO)—totaled just 21 events in April. Public token sales generated only $25.06 million, with activity distributed across multiple blockchains: one round on Solana, five on Ethereum and Base, and two on BNB Chain. BNB Chain was the sole bright spot, achieving 1,269% growth on its April offerings, while most token sales remained underwater.

The slowdown in fundraising and token sales reflects a broader reallocation of crypto investor capital toward alternative sectors, particularly prediction markets and perpetual futures. According to CryptoRank, the shift also reflects changing narrative priorities: while past funding cycles emphasized new Layer 1 and Layer 2 blockchain networks, current investor focus has pivoted to artificial intelligence. However, crypto startups are not perceived as reliable builders of AI products.

CrunchBase data indicates that AI funding remains abundant, with 2026 marking the highest number of unicorn companies in tech history. Major venture firms, including Andreessen Horowitz, which previously backed multiple crypto projects, have redirected capital toward AI and robotics. CryptoRank also notes that seed-stage funding for traditional startups has expanded to $10 million, though venture backers have become more selective, funding fewer projects overall.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.

Related Articles

CEXs Process $19.17T in Spot Crypto Trading in 2025, TradFi Expands with $37B M&A Activity

Gate News message, cryptocurrency exchanges processed $19.17 trillion in spot crypto trading in 2025, while equities reached $155 trillion and foreign exchange markets conducted $9.6 trillion in daily trading. The market has witnessed $37 billion deployed in TradFi M&A by major players, alongside th

GateNews6h ago

Hyperscale Data Reports $5M in Crypto Mining Revenue for Q1 2026

Hyperscale Data (NYSE American: GPUS) disclosed first-quarter 2026 preliminary revenue, with its cryptocurrency mining business generating approximately $5 million, contributing to total company revenue of around $44 million, up 76% year-over-year.

The company plans to divest its diversified

GateNews6h ago

SoFi Reports $1.1B Q1 Revenue, Up 41%, Launches SoFiUSD Stablecoin

According to Businesswire, SoFi Technologies reported record Q1 net revenue of $1.1 billion, up 41% year-over-year, with net income of $167 million, marking its tenth consecutive quarter of GAAP profitability. The fintech company officially launched its full-reserve U.S. dollar stablecoin SoFiUSD

GateNews6h ago

Tokenized RWA Market Reaches $193.2B by End of Q1 2026, Up 256% in 15 Months

According to CoinGecko, the Tokenized Real-World Assets (RWA) market reached $193.2 billion by the end of Q1 2026, up 256% from $54.2 billion at the start of 2025. Tokenized Treasuries led growth, accounting for 67.2% of the market at approximately $130 billion, while Tokenized Commodities rose to $

GateNews8h ago

DeFi Hacks Hit $624.58M in April 2026, Sixth-Largest Loss on Record With Most Incidents

According to DefiLlama, DeFi and on-chain infrastructure hacks caused $624.58 million in losses in April 2026, marking the sixth-largest monthly loss on record. The 23 incidents recorded that month also represent the highest number of attacks in a single month since tracking began in

GateNews11h ago

Galaxy Digital Reports $216M Q1 Loss, Stock Rallies 5% on AI Infrastructure Progress

According to BlockBeats, Galaxy Digital reported a net loss of $216 million in Q1 2026 on April 30, primarily due to a 20% decline in total cryptocurrency market capitalization. The company's crypto asset holdings fell from $1.67 billion at the end of Q4 2025 to $1.36 billion in early

GateNews13h ago